Market Overview

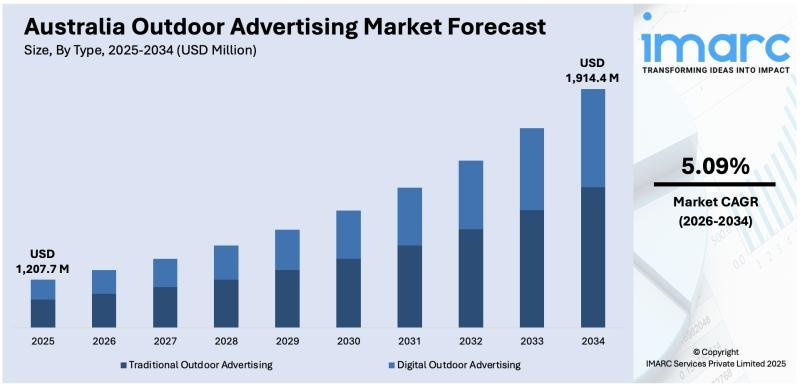

The Australia Outdoor Advertising Market reached a size of USD 1,207.7 Million in 2025 and is projected to reach USD 1,914.4 Million by 2034, growing at a CAGR of 5.09% during the forecast period of 2026-2034. The market is growing through regional expansion, digital innovation, programmatic technology adoption, and multicultural audience engagement – with Australia’s OOH sector having established itself as one of the most digitally advanced and commercially dynamic in the world. Australia’s 2024 OOH revenue growth of 8.1% outperformed even the highly advanced UK market, with DOOH accounting for more than 75% of outdoor revenue – a ratio that positions Australia ahead of most comparable markets in the global transition from traditional static to digital out-of-home advertising. In the first half of 2024, the Australian OOH industry generated AUD 593.1 Million, reflecting an 8% increase compared to the same period in 2023, with DOOH comprising 74.4% of total net media revenue – and the Australian digital out-of-home advertising market is projected to reach AUD 1.27 Billion by 2030, with a CAGR of 10.6% from 2025 to 2030. The market is anchored by three dominant players – oOh!media, which dominates roadside and airport media with a strong digital focus; JCDecaux Australia, which excels in street furniture and large-format billboards; and QMS Media, a leader in premium large-format digital billboards – alongside a growing ecosystem of specialist operators including VMO, Scentre Group’s BrandSpace, Tonic Health Media, Shopper Media Group, and an expanding regional tier of operators including Bishopp Outdoor. Average OOH ad spending per capita in Australia is projected at USD 31.61 in 2025, reflecting the market’s commercial maturity as a mainstream advertising channel. Digital outdoor advertising is the dominant type, billboard advertising leads by segment, and New South Wales leads regionally through Sydney’s density of premium large-format, transport, and retail media inventory.

https://www.imarcgroup.com/australia-outdoor-advertising-market

How AI is Reshaping the Future of the Australia Outdoor Advertising Market:

• 42% of Australian advertising agencies are actively exploring the use of AI in DOOH for audience identification and segmentation – with machine learning models applied to anonymized mobility data, mobile device signals, and facial attribute estimation enabling DOOH operators including JCDecaux and QMS to move beyond panel-level demographic estimates toward real-time, impression-level audience composition measurement that justifies premium pricing for high-dwell-time locations and powers more precise programmatic audience targeting.

• QMS envisions a future where billboards no longer rely on pre-defined playlists but leverage IoT, AI, and real-time data to display the most relevant creative – turning static screens into dynamic, responsive canvases, with AI creative optimization engines analyzing real-time contextual signals including weather, traffic density, time-of-day, nearby events, and local retail sales data to autonomously select and serve the highest-performing creative variant from a brand’s library for each impression opportunity.

• The use of Market Mix Modelling for assessing the effectiveness of pDOOH campaigns has risen from 32% in 2024 to 51% in 2025 – with AI-powered MMM platforms applying machine learning to integrated datasets spanning OOH impression data, retail sales, web traffic, and brand search volume to quantify the incremental contribution of DOOH to business outcomes, providing the ROI attribution clarity that is accelerating budget reallocation from traditional media toward programmatic DOOH.

• MOVE 2.0 – the next generation of Australia’s OOH audience measurement system – launched in 2025 to incorporate visibility and attention metrics, regional audiences for the first time, and coverage of more than 100,000 OOH assets nationally, with AI-powered audience modelling underpinning the system’s ability to estimate impression delivery across vehicular and pedestrian traffic in both metropolitan and regional locations – providing the standardized measurement infrastructure that enables media buyers to plan, optimize, and report on OOH campaigns with the same rigor applied to digital channels.

• oOh!media’s data-led campaign planning and performance suite – unveiled at its annual Outfronts – uses AI to integrate first-party audience data, movement patterns, and campaign exposure data to enable advertisers to target specific audience segments across oOh!’s national network of roadside, retail, airport, café, and office environments, moving OOH from a reach-and-frequency medium to a precision audience targeting channel comparable in measurement sophistication to programmatic digital display.

Request Industry-Focused Sample with Insights & Forecasts

https://www.imarcgroup.com/australia-outdoor-advertising-market/requestsample

Market Trends and Insights

• DOOH Now Dominates Australian OOH Revenue: DOOH accounted for more than 75% of Australian outdoor revenue in 2024 – a higher proportion than most international comparable markets – driven by sustained capital investment in digital screen installation across roadside, retail, transport, and street furniture formats, with approximately 30% of Australia’s outdoor inventory digitised overall, though this proportion falls to around 10% in regional areas, indicating significant remaining headroom for the ongoing digitisation wave that will power revenue growth through the forecast period.

• Programmatic DOOH Transitioning from Experiment to Standard: Australian agencies are increasingly using programmatic DOOH, moving from experimentation to regular consideration in campaign planning – with 81% of agencies now planning OOH, DOOH and pDOOH advertising within the same team, and 68% frequently or sometimes aligning pDOOH buys with digital video activity, while oOh!media reported a significant uptick in programmatic trading across 2024, attributing the growth to its flexibility and omnichannel potential.

• MOVE 2.0 Unlocking Regional Market Investment: The launch of MOVE 2.0 – which includes regional audiences for the first time, covering more than 100,000 OOH assets across the country – is expected to make marketers pay attention to non-metro areas, which currently account for less than 20% of overall OOH media revenue despite being home to 35% of Australia’s population – with the new measurement system creating the audience quantification foundation that will catalyze advertiser investment in regional inventory that has historically been purchased on faith rather than data.

• Retail Media and Health Networks Expanding OOH Environments: Retail media within OOH – including Bunnings’ expansion of in-store large LED screens tapping into Australia’s retail media market, and health networks in hospitals and clinics – is gaining traction as advertisers seek contextually relevant audience touchpoints, with Scentre Group’s BrandSpace, Cartology (Woolworths), and Coles’ media network each operating significant in-store DOOH environments that merge retail media and OOH data capabilities.

• Sustainability Becoming a Competitive Differentiator: JCDecaux has made strides with its Scope 3 carbon measurement tool and a 70% reduction in emissions since 2021, including AUD 2.5 Million in First Nations partnerships, while oOh!media is advancing sustainability with innovations like EcoBanner – a recyclable billboard skin that eliminates landfill waste – and transitioning 14,000 ad panels to renewable energy sources, with sustainability credentials becoming a meaningful differentiator in agency and advertiser site-selection decisions as ESG accountability obligations extend to media investment choices.

Digital outdoor advertising is the dominant type by revenue – anchored by large-format digital roadside billboards, premium digital transit screens, DOOH retail media, and digital street furniture – with digital OOH revenue accounting for 68.5% of total net media revenue year-to-date in 2023, an increase from 57.9% in the comparable prior period, with the proportion continuing to grow toward 75%+ by 2024. Traditional outdoor advertising retains revenue contribution through static roadside billboards, static transit advertising, and traditional street furniture – particularly in regional markets where digitisation penetration remains low at around 10%, creating the inventory base that MOVE 2.0 will progressively bring into mainstream advertiser consideration. Billboard advertising is the largest segment, encompassing both traditional static and large-format digital roadside installations that provide mass metropolitan reach. Transport advertising is the second-largest segment – spanning airports, train stations, bus shelters, and transit carriage panels – with retail, public transport and airports identified as the top areas to watch heading into 2025, with top-tier sites being booked months in advance. Street furniture advertising is the third segment – encompassing bus shelters, kiosks, and pedestrian retail environments – where JCDecaux and oOh! operate the largest national networks. New South Wales leads regionally by revenue, anchored by Sydney’s premium C B D, transport, and airport OOH inventory concentration, with Victoria a strong second through Melbourne’s large commuter transport networks and Westfield retail media environments.

Market Growth Drivers

Surge in Urban Mobility and Public Footfall

Australia’s growing urban population and increasing daily reliance on public transportation – with metropolitan rail patronage in Sydney and Melbourne recovering to and exceeding pre-pandemic levels – is creating expanding out-of-home audience volumes across the transport, retail, and street environment segments that drive OOH revenue growth. Increased demand in transit formats has grown as more Australians return to their offices across the country, according to UM Australia’s head of trading, with urban commuter flows through train stations, bus interchanges, and airport terminals generating high-frequency, captive audience exposures that command premium CPMs from advertisers. The ongoing development of public transport infrastructure – including Sydney Metro expansions, Melbourne Metro Tunnel completion, and Brisbane’s Cross River Rail – is continuously adding new high-quality OOH advertising environments in locations with structurally guaranteed audience volumes, expanding the premium inventory base available to oOh!media, JCDecaux, and QMS across the forecast period. A System1 and JCDecaux study found that 60% of Australian OOH ads resulted in brand recognition, against 50% globally – a performance premium that validates advertisers’ willingness to invest in premium Australian OOH locations and supports sustained market revenue growth.

Advancements in Programmatic Advertising Technology

Programmatic advertising is transforming how outdoor campaigns are planned, purchased, and optimized in Australia – with DOOH programmatic platforms enabling real-time targeting based on audience demographics, weather conditions, traffic flow, time-of-day triggers, and nearby event schedules that deliver relevance and efficiency not achievable through traditional direct-buying processes. JCDecaux CEO Steve O’Connor confirmed sustained investment in programmatic capabilities, noting that programmatic trading enhances campaign agility and enables advertisers to allocate budgets more efficiently, while 83% of Australian agencies used pDOOH for brand awareness objectives in 2025, and 68% aligned pDOOH buys with digital video activity – with the use of Market Mix Modelling for pDOOH effectiveness assessment rising from 32% in 2024 to 51% in 2025. Australia’s programmatic DOOH ecosystem encompasses 26,000 available screens across major cities and environments, with the IAB Australia DOOH Council – comprising JCDecaux, Google, The Trade Desk, WPP Media, oOh!media, Scentre Group, and others – actively developing the industry standards, buyer education resources, and measurement frameworks that will support continued pDOOH investment growth through the forecast period.

Strong Brand Impact and Regional Expansion

Australia’s outdoor advertising market is experiencing a dual growth engine – combining the sustained premium of large-format brand-building environments in metropolitan centers with an accelerating expansion wave into regional markets that have historically been underinvested relative to their population share. In December 2024, Bishopp Outdoor Advertising launched 126 new OOH sites across Australia – including 14 digital units – with partnerships at Hobart and Launceston airports, the Port of Airlie cruise terminal, and nearly 100 advertising spots in regional NSW through a collaboration with the Australian Rail Track Corporation, demonstrating the commercial viability of regional OOH expansion supported by measurement, programmatic capability, and strategic location selection. Regional markets account for less than 20% of overall OOH media revenue despite being home to 35% of Australia’s population – a structural under-representation that MOVE 2.0’s regional audience measurement and the ongoing digitisation of regional inventory are set to progressively correct throughout the forecast period, with regional OOH representing one of the market’s highest-growth opportunities for operators, national advertisers, and government campaigns seeking to reach populations outside Australia’s major metropolitan centers.

Market Segmentation

Type Insights:

• Traditional Outdoor Advertising

• Digital Outdoor Advertising

Segment Insights:

• Billboard Advertising

• Transport Advertising

• Street Furniture Advertising

• Others

Regional Insights:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Recent News and Developments

• August 2025: The IAB Australia DOOH Council released an updated Programmatic DOOH Buyers Guide – a comprehensive 20-page resource covering buying methods, targeting strategies, creative considerations, measurement frameworks, and verification standards – alongside research findings from 116 Australian agencies showing that 83% are using pDOOH for brand awareness, 42% are exploring AI for audience identification, and Market Mix Modelling adoption for pDOOH effectiveness assessment rose from 32% to 51% year-on-year.

• May 2025: Wildstone entered into partnerships with oOh!media and Gawk Outdoor to manage advertising operations across its newly acquired portfolio of 52 sites in regional Victoria – comprising 14 digital billboards and 38 traditional displays in Geelong, Ballarat, Bendigo, Shepparton, and Wangaratta – marking a significant consolidation of regional OOH inventory management and expanding the national programmatic DOOH coverage available through major demand-side platforms.

• April 2025: VMO unveiled Dimensions – an innovative collection of outdoor screen solutions aimed at redefining brand interaction and audience engagement through impactful creative formats – launching a new generation of large-format DOOH screens designed to revolutionize how campaigns come alive and deliver immersive brand experiences that extend creative possibilities beyond conventional billboard and transit formats.

• April 2025: Tourism Australia executed a three-week large-format OOH campaign across Delhi NCR and Mumbai – managed by Greenline Glo, featuring digital screens, large-format billboards, and high-visibility mall facades showcasing “The view’s even better down under” – targeting affluent Indian consumers in airports, malls, and corporate hubs to build Australia’s destination appeal among the rapidly growing outbound Indian travel market.

• February 2025: Multicultural Outdoor (MCO) launched Australia’s first DOOH network targeting diverse communities with in-language advertisements across Sydney and Melbourne – expanding from 179 to 250 screens – enhancing multicultural audience outreach, improving inclusivity in outdoor media, and opening a new addressable audience segment for brands and government campaigns seeking to engage Australia’s linguistically diverse communities.

• October 2024: oOh!media and ANZ launched Australia’s largest 3D Out-of-Home campaign across 2,100 digital screens nationwide – targeting multiple environments including roadside, retail, and transit – establishing a new creative benchmark for large-scale 3D DOOH production in Australia and demonstrating the scalable commercial viability of immersive 3D technology as a standard creative format for nationally coordinated OOH campaigns.

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

Ask analyst for your customized sample:

https://www.imarcgroup.com/request?type=report&id=32279&flag=F

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC’s offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.