satellite-to-phone service market

Leander, Texas and Tokyo, Japan – Dec.10.2025

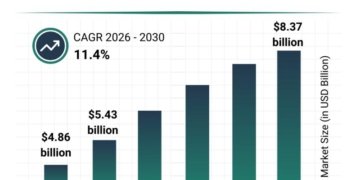

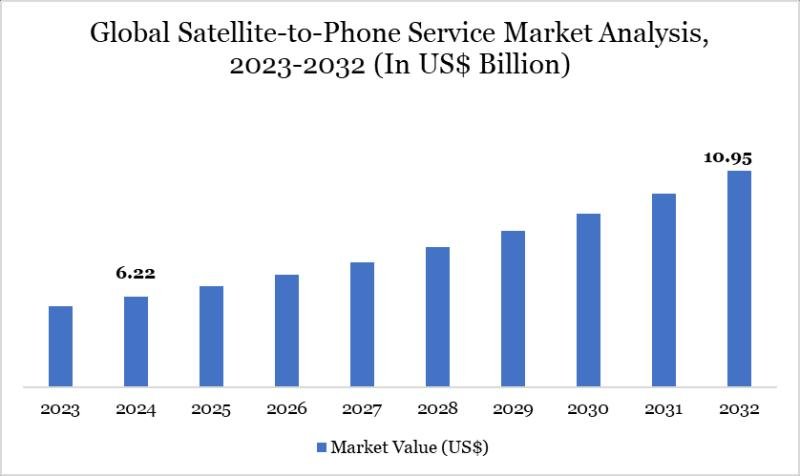

As per DataM intelligence research report” Global satellite-to-phone service market size reached US$ 6.22 billion in 2024 and is expected to reach US$ 10.95 billion by 2032, growing with a CAGR of 7.32% during the forecast period 2025-2032.” Direct-to-device connectivity and universal coverage needs are propelling satellite-to-phone communication services.

Download your exclusive sample report today: (corporate email gets priority access):

https://www.datamintelligence.com/download-sample/satellite-to-phone-service-market?Prasad

United States: Recent Industry Developments

✅ In November 2025, SpaceX launched the first full constellation of “Starlink Direct to Cell” satellites The service enables text and voice coverage for T-Mobile users in U.S. dead zones It eliminates cellular blackspots across the continental United States

✅ In October 2025, AST SpaceMobile successfully completed a 5G video call via satellite with AT&T The demonstration proved the high-bandwidth capability of their BlueWalker satellites It paves the way for broadband-speed connectivity from space

✅ In September 2025, Apple announced the expansion of “Emergency SOS via Satellite” to support roadside assistance The feature connects stranded drivers with help even without a cellular signal It enhances the safety value proposition of the iPhone ecosystem

✅ In August 2025, The FCC adopted new rules to streamline the leasing of spectrum for satellite-to-phone services The regulatory framework encourages collaboration between terrestrial carriers and satellite operators It accelerates the commercial rollout of space-based connectivity

Japan: Recent Industry Developments

✅ In December 2025, KDDI launched “Starlink Direct to Cell” service for its au subscribers in Japan The service provides coverage in mountainous regions and remote islands previously unconnected It significantly improves disaster communication resilience in Japan

✅ In November 2025, Rakuten Mobile partnered with AST SpaceMobile to test satellite coverage over Mt. Fuji The test aims to provide continuous connectivity for climbers and tourists It showcases the utility of the service in Japan’s rugged terrain

✅ In October 2025, SoftBank Corp announced a strategic investment in a satellite IoT startup The investment focuses on connecting remote sensors and devices via satellite It expands the “Non-Terrestrial Network” (NTN) strategy beyond smartphones

✅ In September 2025, The Japanese government allocated new frequency bands for satellite-direct communication The allocation aligns with global standards to facilitate international roaming It ensures Japan remains at the forefront of 6G and NTN development

Satellite-to-Phone Service Market: Drivers

Satellite-to-phone service is gaining traction as demand for global connectivity and emergency communication grows, particularly in remote, maritime, and disaster-prone areas. These services allow direct communication via satellite networks without reliance on terrestrial infrastructure, supporting voice, SMS, and emerging data services. Technological advancements in low-Earth orbit (LEO) satellites, network latency reduction, and handset design are expanding usability and affordability. Regulatory approvals and spectrum allocation are key enablers for service deployment.

Growth is fueled by demand from outdoor enthusiasts, maritime operators, government agencies, and industrial enterprises requiring resilient connectivity. Integration with IoT applications, GPS tracking, and disaster response systems enhances functionality and market potential. Partnerships between satellite operators, telecom providers, and handset manufacturers facilitate broader adoption. With increasing global mobility and need for reliable communication, satellite-to-phone services are positioned for long-term expansion.

Get Customization in the report as per your requirements: https://www.datamintelligence.com/customize/satellite-to-phone-service-market?Prasad

Satellite-to-Phone Service Market: Major Players

SpaceX (Starlink), Iridium Communications Inc., Globalstar Inc., Inmarsat, Viasat Inc., Skylo Technologies, AST SpaceMobile, Qualcomm Technologies, Inc., T-Mobile US, Inc. and Apple Inc.

Segment Covered in the Satellite-to-Phone Service Market:

By Service Type

Service types include data services 40%, voice services 25%, messaging services 20%, and emergency services 15%, with data services dominating due to growing user demand for broadband-like connectivity and IoT telemetry. Voice remains vital for basic connectivity and legacy use, while messaging is popular for low-bandwidth, low-cost communication. Emergency services are critical for safety, disaster response, and regulatory mandates. Rising consumer and enterprise demand for ubiquitous connectivity drives growth across all service types.

By Technology

Technology splits into direct-to-device (D2D) communication 55% and relay-based communication 45%, with D2D leading because it enables simpler, lower-latency connections to standard handsets without intermediate terminals. Relay-based systems remain important for capacity, beamforming, and coverage in challenging environments. Both architectures coexist as operators balance cost, latency, and spectrum efficiency. Advances in LEO constellations and handset chipsets accelerate D2D adoption.

By Frequency Band

Frequency band segmentation is L-Band 35%, S-Band 15%, Ku-Band 20%, Ka-Band 20%, and others 10%, with L-Band dominating for handset-friendly services due to penetration and mature ecosystems. Ku and Ka support higher-throughput data links and backhaul, while S-Band is emerging for mid-capacity consumer and IoT services. Higher bands enable greater bandwidth but require more complex ground and terminal hardware. Spectrum strategy and regulatory access shape band selection and service economics.

By End-User

End-users include consumer 30%, government & defense 20%, maritime 15%, aviation 10%, energy & utilities 10%, transportation & logistics 10%, and others 5%, with consumer services driving mass adoption for remote communication and safety. Government & defense demand secure, resilient comms for critical missions. Maritime and aviation use cases prioritize certified voice/data for safety and operations. Industry verticals such as energy and transport adopt satellite-to-phone for remote telemetry, worker safety, and redundancy.

Regional Analysis

North America – 35% Share

North America leads with 35% share driven by early commercial rollouts, high disposable income, strong satellite operator presence, and regulatory support in the U.S. and Canada. Consumer uptake and government/defense contracts are major growth drivers. D2D services and L-Band offerings are widely deployed. Robust retail channels and handset partnerships accelerate market expansion.

Europe – 25% Share

Europe holds 25% share supported by dense aviation and maritime routes, progressive spectrum allocation, and growing consumer interest in fallback connectivity across Germany, UK, France, and the Nordics. Government procurement and enterprise IoT use cases push demand. Relay and Ka/Ku solutions complement L-Band consumer offerings. Cross-border roaming and regulatory alignment influence operator strategies.

Asia-Pacific – 20% Share

Asia-Pacific accounts for 20% share driven by vast rural populations, maritime fleets, and rapid mobile adoption in China, India, Japan, Australia, and Southeast Asia. Consumer and enterprise demand for remote connectivity and disaster resilience fuels growth. Mix of D2D L-Band services and higher-throughput Ku/Ka links serve diverse use cases. Regional partnerships and local handset certifications are key to scale.

Latin America – 8% Share

Latin America holds 8% share with growing adoption in Brazil, Mexico, and Argentina for rural connectivity, maritime operations, and emergency services. L-Band D2D and hybrid relay deployments are common. Consumer uptake is rising where terrestrial coverage is weak. Government programs and natural-disaster resilience planning support market uptake.

Middle East – 7% Share

The Middle East records 7% share driven by energy & utilities, maritime logistics, and government use in UAE, Saudi Arabia, and Qatar. High-value enterprise and government contracts favor resilient satellite-to-phone solutions. Ku/Ka links are used for high-capacity backhaul while L-Band supports handset services. Strategic investments and infrastructure projects spur adoption.

Africa – 5% Share

Africa holds 5% share due to large underserved rural areas and rising demand for basic voice/data and emergency comms across South Africa, Nigeria, Kenya, and Egypt. L-Band D2D solutions are particularly attractive for affordability and penetration. Maritime, mining, and humanitarian use cases lead commercial uptake. Subsidies, donor programs, and telco partnerships help expand reach.

Purchase this report before year-end and unlock an exclusive 30% discount:

https://www.datamintelligence.com/buy-now-page?report=satellite-to-phone-service-market

(Purchase 2 or more Repots and get 50% Discount)

Request for 2 Days FREE Trial Access:

https://www.datamintelligence.com/reports-subscription?Prasad

✅ Competitive Landscape

✅ Technology Roadmap Analysis

✅ Sustainability Impact Analysis

✅ KOL / Stakeholder Insights

✅ Consumer Behavior & Demand Analysis

✅ Import-Export Data Monitoring

✅ Live Market & Pricing Trends

Have a look at our Subscription Dashboard:

https://www.youtube.com/watch?v=x5oEiqEqTWg

Contact Us –

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: Sai.k@datamintelligence.com

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

About Us –

DataM Intelligence is a Market Research and Consulting firm that provides end-to-end business solutions to organizations from Research to Consulting. We, at DataM Intelligence, leverage our top trademark trends, insights and developments to emancipate swift and astute solutions to clients like you. We encompass a multitude of syndicate reports and customized reports with a robust methodology.

Our research database features countless statistics and in-depth analyses across a wide range of 6300+ reports in 40+ domains creating business solutions for more than 200+ companies across 50+ countries; catering to the key business research needs that influence the growth trajectory of our vast clientele.

This release was published on openPR.