Serverless Computing Market

The Global Serverless Computing Market reached US$ 9.3 Billion in 2023 and is expected to reach US$ 40.9 Billion by 2031, growing with a CAGR of 20.6% during the forecast period 2024-2031.

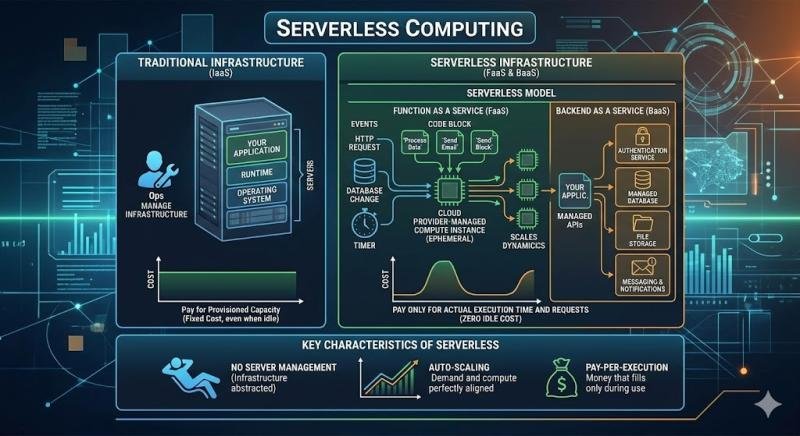

The market is rapidly expanding as enterprises and cloud providers shift toward event-driven, pay-per-use architectures, fueled by the explosion in AI workloads, microservices adoption, and the need for scalable DevOps. This growth reflects a fundamental change in computing paradigms, moving away from traditional server management toward fully managed, auto-scaling platforms that optimize costs and accelerate innovation in real-time applications like edge AI and IoT.

Download Executive Sample Report (Get Higher Priority for Corporate Email ID):- https://www.datamintelligence.com/download-sample/serverless-computing-market?ram

Key Industry Developments

United States:

✅ February 2026: AWS launched Lambda SnapStart 2.0, a major upgrade reducing cold start times by 90% for Java and .NET functions through advanced snapshot optimization and pre-warming techniques, enabling near-instantaneous scaling for high-throughput enterprise workloads. This advancement supports mission-critical applications in finance and e-commerce by minimizing latency in event-driven architectures.

✅ January 2026: Google Cloud introduced Cloud Run V2 with built-in AI inference endpoints, allowing seamless serverless deployment of machine learning models with automatic GPU provisioning and real-time auto-scaling. The update integrates Vertex AI for predictive scaling, cutting deployment times by 70% for data-intensive US enterprises.

✅ November 2025: Microsoft Azure announced Functions Durable Objects, a new R&D breakthrough for stateful serverless workflows using globally distributed storage, improving orchestration reliability for complex microservices by 50% without traditional database dependencies. This targets US developers building resilient, multi-region applications in gaming and IoT sectors.

Japan:

✅ December 2025: NTT Communications unveiled Serverless Edge for 5G, a Tokyo-based product launch combining FaaS with edge computing nodes optimized for low-latency IoT in smart cities, leveraging hybrid cloud for industrial automation with 40% faster response times. The initiative aligns with Japan’s digital transformation policies, focusing on Kansai region’s manufacturing hubs.

✅ October 2025: Fujitsu released a serverless platform update for quantum-inspired optimization, integrating annealing algorithms into Functions-as-a-Service for rapid R&D prototyping in logistics and finance, reducing computation costs by 60% for Japanese enterprises. This advancement supports national AI initiatives with scalable, pay-per-use quantum simulation.

✅ September 2025: Sakura Internet expanded its serverless offerings with AI-optimized cold start mitigation, a Hokkaido data center upgrade providing sub-100ms invocation for e-commerce workloads during peak seasons, enhancing scalability for Japan’s booming online retail sector.

Strategic Acquisitions and Partnerships

✅ Akamai Technologies acquired Fermyon, a serverless WebAssembly company, on December 1, 2025, enhancing its edge computing capabilities and serverless platform offerings for scalable, lightweight deployments.

Key Players:

Google LLC | Alibaba Cloud | CA Technologies | Microsoft Corporation | Oracle Corporation | Dynatrace | Fiorano Software Inc. | Joyent Inc. | Modubiz Ltd. | NTT Data Corporation

Strategic Leadership Analysis: Top 5 Players in Serverless Computing Market 2026

-Google LLC: Launched the serverless version of Cloud Run with integrated AI model serving, enabling seamless scaling for generative AI workloads and pay-per-use inference to optimize developer productivity in event-driven architectures.

-Microsoft Corporation: Advanced Azure Functions with durable orchestration and native WebAssembly support, delivering enhanced cold start performance and hybrid container execution for mission-critical enterprise serverless applications.

-Alibaba Cloud: Introduced the serverless PAI-Elastic Algorithm Service (EAS), providing cost-efficient deployment of LLMs and image generation models with up to 50% inference cost reduction through on-demand computing resources.

-Oracle Corporation: Expanded Oracle Functions with GraalVM native compilation and Fn Project integration, offering sub-millisecond latency and multi-language runtime flexibility for high-throughput serverless microservices in cloud-native environments.

-NTT Data Corporation: Debuted the serverless edge computing platform with zero-cold-start functions and integrated API gateway, enabling low-latency processing for IoT and 5G applications across distributed hybrid cloud deployments.

Speak to Our Analyst and Get Customization in the report as per your requirements: https://www.datamintelligence.com/customize/serverless-computing-market?ram

Main Drivers and Trends Shaping the Future of Serverless Computing Market

-Cost Efficiency: Serverless architectures enable pay-per-use models that eliminate idle infrastructure costs, allowing organizations to scale resources dynamically and reduce operational expenses significantly.

-Scalability Demands: Real-time event-driven computing supports microservices and cloud-native apps, meeting enterprise needs for instant workload scaling without server provisioning.

-AI/ML Integration: Serverless platforms power machine learning pipelines and predictive analytics, accelerating deployment of intelligent applications across industries like healthcare and finance.

-Edge Computing Synergy: Bringing serverless execution closer to data sources cuts latency for IoT and real-time analytics, driving adoption in smart infrastructure and autonomous systems.

-Global Digital Shift: Rapid cloud adoption in Asia-Pacific and emerging markets fuels growth through urbanization, industrialization, and demand for agile developer tools.

-Market Hurdles: Cold start latencies, vendor lock-in risks, and maturing stateful function support pose constraints, alongside security challenges in multi-tenant environments.

Regional Insights:

-North America: 40% (Largest share, led by hyperscaler dominance from AWS, Azure, and Google Cloud, plus mature cloud adoption in tech hubs like Silicon Valley).

-Asia Pacific: 25% (Fastest growing, driven by rapid digitalization, cloud infrastructure expansion in China and India, and high mobile internet penetration).

-Europe: 18% (Strong growth from BFSI digital transformation, GDPR-compliant cloud modernization, and event-driven architecture adoption).

Market Opportunities & Challenges: Serverless Computing Market 2026

-Opportunities: A “Cloud-Native Acceleration” favors event-driven workloads; AI inferencing and microservices modernization enable seamless scaling for real-time IoT telemetry and streaming analytics. SME digitalization via turnkey platforms and Asia-Pacific ecosystem expansions spurred by low-latency data processing create agile entry points for rapid product launches and hybrid deployments.

-Challenges: Cold start latencies and vendor lock-in complexities hinder mission-critical adoption, while fragmented observability across multi-cloud environments demands advanced tooling. Success requires mastering concurrency limits and architecturally complex state management in distributed systems.

Purchase Corporate License | Market Intelligence: https://www.datamintelligence.com/buy-now-page?report=serverless-computing-market?ram

Market Segmentation Analysis:

-By Services: API Management Services Lead Integration Needs

API Management Services dominate at 30% share in 2024, enabling seamless developer access and microservices orchestration in scalable apps.

Monitoring Services follow at 25%, providing real-time performance insights and troubleshooting for serverless workloads.

Integration Services (20%), Security (15%), Support & Maintenance (5%), and Others (5%) support ecosystem reliability, with security rising amid data threats.

-By Deployment: Public Cloud Commands Scalability

Public Cloud holds 70% share, favored for pay-per-use elasticity and hyperscaler ecosystems like AWS Lambda and Azure Functions.

Private Cloud takes 30%, preferred by enterprises for compliance and data sovereignty in regulated sectors.

-By Enterprise Size: Large Enterprises Drive Adoption

Large Enterprises capture 65% share, leveraging serverless for complex, high-volume workloads and cost optimization.

Small and Medium Enterprises (SMEs) account for 35%, benefiting from low upfront costs and rapid prototyping.

-By Application: Web & Mobile Apps Top Usage

Web and Mobile Applications lead at 50% share, powering dynamic, event-driven UIs with auto-scaling.

IoT follows at 50%, enabling edge processing for real-time data streams in connected devices.

-By End-User: IT & Telecom Spearheads Innovation

IT and Telecom command 25% share, using serverless for 5G networks and agile DevOps.

BFSI (20%), Retail (15%), Healthcare (15%), Manufacturing (10%), Media & Entertainment (10%), and Others (5%) adopt for fintech, e-commerce personalization, and streaming scalability.

Unlock 360° Market Intelligence with DataM Subscription Services: https://www.datamintelligence.com/reports-subscription?ram

Power your decisions with real-time competitor tracking, strategic forecasts, and global investment insights all in one place.

✅ Competitive Landscape

✅ Sustainability Impact Analysis

✅ KOL / Stakeholder Insights

✅ Unmet Needs & Positioning, Pricing & Market Access Snapshots

✅ Market Volatility & Emerging Risks Analysis

✅ Quarterly Industry Report Updated

✅ Live Market & Pricing Trends

✅ Import-Export Data Monitoring

Have a look at our Subscription Dashboard: https://www.youtube.com/watch?v=x5oEiqEqTW

Contact Us –

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: Sai.k@datamintelligence.com

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

About Us –

DataM Intelligence is a Market Research and Consulting firm that provides end-to-end business solutions to organizations from Research to Consulting. We, at DataM Intelligence, leverage our top trademark trends, insights and developments to emancipate swift and astute solutions to clients like you. We encompass a multitude of syndicate reports and customized reports with a robust methodology.

Our research database features countless statistics and in-depth analyses across a wide range of 6300+ reports in 40+ domains creating business solutions for more than 200+ companies across 50+ countries; catering to the key business research needs that influence the growth trajectory of our vast clientele.

This release was published on openPR.