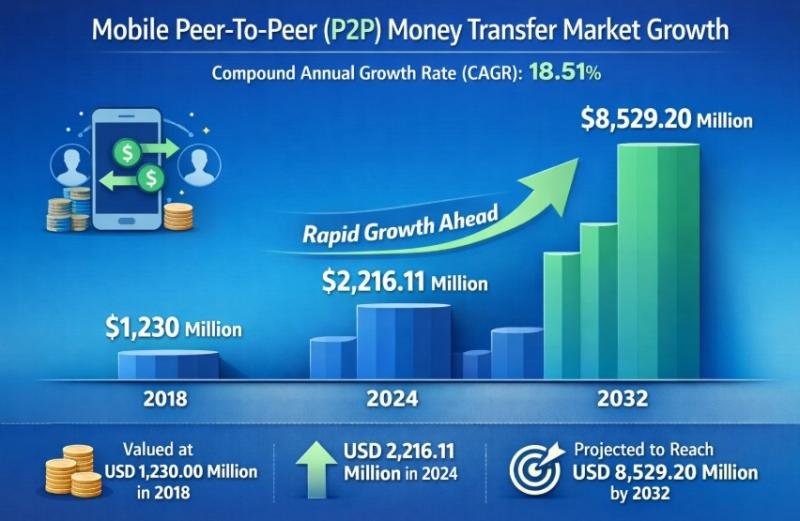

The Mobile Peer-To-Peer (P2P) Money Transfer market has shifted from a convenience-driven payment option into a core layer of the modern digital economy. As smartphones, mobile wallets, QR codes, and real-time payment rails become mainstream, consumers and small businesses increasingly expect instant, low-friction money movement across apps and borders. Reflecting this rapid transformation, the Mobile Peer-To-Peer (P2P) Money Transfer market size was valued at USD 1,230.00 million in 2018, grew to USD 2,216.11 million in 2024, and is anticipated to reach USD 8,529.20 million by 2032, at a robust CAGR of 18.51% during the forecast period. This growth trajectory is powered by the expansion of cashless ecosystems, rising digital commerce, surging travel recovery, and the growing role of embedded finance in everyday apps.

Browse the full Report at https://www.credenceresearch.com/report/mobile-p2p-money-transfer-market

Mobile P2P money transfer solutions allow users to send and receive money using smartphones, typically linked to bank accounts, cards, or stored wallet balances. Over time, these platforms have expanded well beyond “send money to friends” use cases. Today’s leading services combine P2P transfers with merchant acceptance, bill payments, subscriptions, transit payments, cross-border remittances, and even financial services such as savings, investing, and credit. In many markets, P2P has become a gateway into broader digital financial inclusion by offering a simple, app-first entry point for users who may be underserved by traditional banking.

In mature regions, the market is driven by lifestyle convenience and deep integration with retail and platform commerce. In emerging economies, growth is further amplified by rapid smartphone penetration, government-backed digital rails, and merchant digitization-from small neighborhood shops to large retail chains. The ecosystem is also being shaped by partnerships between wallet providers, banks, payment networks, telecom operators, and technology platforms, creating powerful distribution networks and strong user retention.

Get Free PDf Sample Request: https://www.credenceresearch.com/report/mobile-p2p-money-transfer-market#request_sample

1) Shift toward cashless transactions and wallet-led behavior

Consumers increasingly prefer contactless and app-based payments due to speed, ease, rewards, and improved budgeting visibility. As daily payment behavior shifts from cash to digital, P2P becomes a natural extension-especially for shared expenses, peer reimbursements, and quick transfers for services.

2) Real-time payment infrastructure and interoperability

The rollout of instant payment systems and better API-based banking connectivity has improved transaction speed and reliability. Interoperability between banks and wallets reduces friction, enabling P2P services to expand their addressable user base and increase transaction frequency.

3) Expansion of use cases beyond personal transfers

P2P is now used for gig worker payouts, small merchant payments, event ticket sharing, group travel expenses, donations, and “social commerce” transactions. This broadening of use cases boosts transaction volume and creates additional revenue opportunities through merchant fees, value-added services, and premium subscriptions.

4) Cross-border demand and global mobility

As international travel resumes and cross-border commerce expands, consumers want simple ways to split expenses abroad, pay local merchants, and transfer funds internationally. Multi-currency wallets and low-cost FX-enabled transfer platforms are benefiting from this trend.

5) Platformization of payments (super-apps and embedded finance)

Payments increasingly live inside ecosystems such as messaging apps, e-commerce platforms, ride-hailing services, and banking super-apps. When P2P transfers are embedded into high-frequency apps, user engagement and retention rise sharply.

Get Free PDf Sample Request: https://www.credenceresearch.com/report/mobile-p2p-money-transfer-market#request_sample

Security, fraud, and trust management

P2P platforms are attractive targets for social engineering, account takeovers, and synthetic identity fraud. Providers must invest heavily in risk engines, authentication, behavioral analytics, and customer education. A single high-profile security incident can damage brand trust and slow adoption.

Regulatory complexity and compliance costs

Payments are highly regulated, and requirements vary across countries-covering KYC/AML, transaction monitoring, data privacy, consumer protection, and reporting obligations. For cross-border transactions, providers face additional scrutiny related to sanctions screening and remittance rules.

Monetization pressure and competitive pricing

Many P2P services compete on free or low-cost transfers, making monetization dependent on scale and adjacent services (merchant payments, instant withdrawals, FX, subscriptions, lending, and interchange). Maintaining margins while keeping users happy is a major strategic balancing act.

Browse the full Report at https://www.credenceresearch.com/report/mobile-p2p-money-transfer-market

Infrastructure and reliability expectations

As consumers treat P2P like a utility, downtime is unacceptable. Providers must ensure resiliency, low latency, and strong customer support-especially during peak periods, holidays, and large events when payment volumes surge.

Mobile Peer-To-Peer (P2P) Money Transfer Market Segmentations

By Type

Remote Payment

Remote payments dominate many P2P flows because they enable transfers without physical proximity. Users can send money to friends, family, or service providers anywhere, anytime. Remote payments also support online commerce, bill splitting, subscription-like reimbursements, and digital gifting. As digital lifestyles and gig work expand, remote payment volume is expected to remain the largest contributor to market growth.

Proximity Payment

Proximity payments are driven by in-person transactions using technologies such as QR codes, NFC (tap-to-pay), and Bluetooth-based solutions. Adoption is especially strong where QR acceptance networks have scaled quickly and where merchants prefer low-cost acceptance compared to traditional card infrastructure. Proximity P2P often overlaps with merchant payments, creating a pathway from “paying a friend” to “paying a store,” which strengthens platform stickiness.

By Application

Retail

Retail is a major growth engine as P2P apps evolve into full wallet ecosystems. Consumers increasingly use P2P wallets to pay at checkout, redeem rewards, access offers, and manage spending. Small merchants benefit from easier onboarding and low hardware requirements (especially for QR), helping drive adoption across urban and semi-urban areas.

Travel and Hospitality

Travel and hospitality applications are rising due to group travel payments, expense splitting, tipping, and quick settlement for bookings and services. P2P-enabled wallets that support multi-currency balances and competitive FX rates are well-positioned to capture international travel spending, particularly among younger, app-native consumers.

Transportation and Logistics

This segment includes ride-hailing, last-mile delivery, tolls, transit payments, and peer payments related to moving goods and people. P2P solutions also play a growing role in instant payouts to gig workers and drivers, improving workforce satisfaction and reducing cash handling risks for platforms.

By Geography

North America (U.S., Canada, Mexico)

North America remains a key market due to high smartphone penetration, mature digital banking, and widespread consumer familiarity with P2P payments. The U.S. continues to lead adoption through strong brand ecosystems and bank-led networks, while Canada and Mexico present opportunities tied to interoperability, remittances, and expanding mobile wallet usage.

Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

Europe’s market is shaped by strong regulatory frameworks, open banking progress, and fast-growing fintech ecosystems. Cross-border movement within the region, international commerce, and multi-currency needs support demand for low-cost transfers and wallet services. Competitive intensity is high, pushing innovation in user experience, fees, and value-added financial products.

Asia Pacific (China, Japan, India, South Korea, South-east Asia, Rest of Asia Pacific)

Asia Pacific is a powerhouse for mobile payments, with broad adoption of QR and wallet-based ecosystems. The region benefits from large populations, high mobile engagement, and strong merchant acceptance in many countries. Super-app ecosystems and domestic payment rails accelerate user growth, and the region is expected to remain one of the most dynamic in terms of innovation and transaction volume.

Latin America (Brazil, Argentina, Rest of Latin America)

Latin America is witnessing rapid growth due to digitization of commerce, expansion of instant payment systems, and strong demand for accessible financial services. P2P adoption is closely linked to mobile-first banking and fintech growth, with significant potential in underbanked populations and informal retail.

Middle East & Africa (GCC Countries, South Africa, Rest of Middle East and Africa)

This region’s growth is supported by rising smartphone use, expanding fintech ecosystems, and a strong remittance corridor presence. Wallets that solve cross-border transfer pain points and enable easy local merchant payments can scale rapidly-especially where governments and regulators support digital transformation.

Browse the full Report at https://www.credenceresearch.com/report/mobile-p2p-money-transfer-market

Key player analysis

The competitive landscape includes global technology platforms, fintech leaders, and bank-led networks. Key success factors include user trust, transfer speed, merchant acceptance, ecosystem partnerships, compliance strength, and the ability to monetize through adjacent services.

PayPal (Venmo): Strong brand recognition and a broad user base, with expanding merchant integration and social-style payment features that drive engagement.

Block, Inc. (Cash App): Differentiates through ecosystem breadth, including consumer finance features and strong appeal among younger demographics.

Zelle: A bank-connected network that emphasizes fast transfers within the banking ecosystem, supporting broad reach through partner institutions.

Google Pay: Benefits from Android distribution, deep platform integration, and growing acceptance across P2P and merchant payments.

Apple Pay: Leverages device ecosystem and security positioning, supporting strong adoption among iOS users and premium segments.

Samsung Pay: Combines device-based distribution with contactless and wallet features, supporting both P2P and proximity payments.

Alipay: A dominant player in wallet-led commerce with extensive merchant acceptance and value-added services.

WeChat Pay (Tencent): Deeply embedded in messaging and daily life, enabling frictionless P2P and merchant flows in super-app contexts.

Wise (formerly TransferWise): Focused on transparent, low-cost cross-border transfers, multi-currency accounts, and strong FX capabilities.

Revolut: Combines P2P with multi-currency wallets, cards, and lifestyle finance features, targeting frequent travelers and digital-first users.

Get Free PDf Sample Request: https://www.credenceresearch.com/report/mobile-p2p-money-transfer-market#request_sample

Recent developments shaping the market

The market continues to evolve through strategic partnerships, regulatory enhancements, security upgrades, and expansion into adjacent financial services. Common themes in recent developments include:

Interoperability improvements between banks and wallets to increase reach and reduce transfer friction.

Stronger fraud prevention using AI-based risk scoring, device intelligence, and real-time behavioral analytics.

Expansion into merchant ecosystems, enabling P2P apps to capture both peer and checkout transactions.

Growth in cross-border capabilities, including faster settlement, better FX transparency, and multi-currency wallets.

Embedded finance partnerships that integrate P2P into commerce platforms, travel apps, and gig worker ecosystems.

Future outlook: where the opportunities are

With an anticipated market value of USD 8,529.20 million by 2032, the Mobile P2P money transfer space is expected to remain among the fastest-growing segments in digital payments. The biggest opportunities will likely emerge in:

Merchant enablement and micro-business payments, where simplified onboarding can scale acceptance quickly.

Cross-border transfers and multi-currency wallets, especially for travel, remittances, and international freelancers.

AI-driven fraud prevention and user protection, improving trust while reducing operational losses.

Financial inclusion expansion, by providing wallet-first access to payments, savings, and credit products.

Platform-led distribution, where super-apps and operating system integrations reduce customer acquisition cost and increase engagement.

Conclusion

Mobile Peer-To-Peer (P2P) money transfers have become foundational to modern digital commerce and daily financial life. The market’s growth-from USD 1,230.00 million in 2018 to USD 2,216.11 million in 2024, and projected to reach USD 8,529.20 million by 2032 at a CAGR of 18.51%-highlights a clear long-term shift toward instant, mobile-first, and ecosystem-integrated payments. As providers strengthen security, expand interoperability, and broaden services beyond simple transfers, P2P platforms will continue evolving into comprehensive digital finance hubs-supporting retail, travel, transportation, and increasingly, cross-border money movement at scale.

Browse the full Report at https://www.credenceresearch.com/report/mobile-p2p-money-transfer-market

Contact US:

Credence Research Inc, Tower C-1105 , S 25, Akash Tower,

Vishal Nahar, Pimple Nilakh, Haveli,

Pune – 411027, India

India – +91 6232 49 3207

sales@credenceresearch.com

http://www.credenceresearch.com

About US:

Credence Research is a leading international provider of market intelligence and a key component in the due diligence process. We deliver high-quality, extensive, deep-dive reports that empower leaders and investors to make informed decisions and mitigate risks. Our strategic insights, based on extensive research frameworks and advanced data modeling, provide authoritative primary sources for evaluating market performance and potential across a wide range of industries.

This release was published on openPR.