IoT Telecom Services Market

According to a new study by DataHorizzon Research, the IoT telecom services market is projected to grow at a CAGR of 34.28% from 2025 to 2033. The accelerating global rollout of 5G network infrastructure, surging enterprise demand for low-latency massive machine-type communication connectivity, and the rapid proliferation of connected device deployments across industrial, automotive, healthcare, and smart city applications are collectively driving unprecedented growth across the IoT telecom services market worldwide. Telecom operators are aggressively repositioning their service portfolios – moving beyond traditional voice and broadband revenues toward managed IoT connectivity, edge network services, eSIM provisioning, and IoT platform-as-a-service offerings that generate recurring, high-margin enterprise revenue streams. As the number of globally connected IoT devices approaches 30 billion and enterprises demand carrier-grade connectivity management at scale, the IoT telecom services market is emerging as the foundational infrastructure layer of the global digital economy with compelling long-term growth fundamentals for investors, operators, and technology ecosystem partners.

IoT Telecom Services Market Key Growth Drivers and Demand Factors

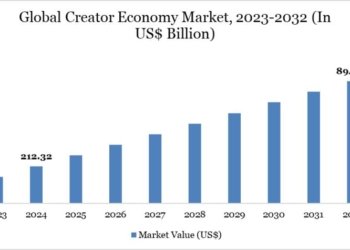

The IoT telecom services market was valued at USD 41.88 billion in 2024 and is projected to reach USD 798.50 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 34.28% from 2025 to 2033.

The IoT telecom services market is experiencing structural demand acceleration shaped by a powerful intersection of network technology advancement, enterprise digitalization urgency, and regulatory spectrum policy evolution that is collectively expanding both the connected device base and the average revenue per IoT connection across operator portfolios. The most consequential near-term driver is the accelerating commercialization of 5G standalone network architecture, which unlocks network slicing, ultra-reliable low-latency communication, and massive IoT device density capabilities that were technically unachievable on 4G LTE infrastructure – fundamentally expanding the addressable application scope of the IoT telecom services market.

Low-power wide-area network technologies, including NB-IoT and LTE-M, are simultaneously driving volume growth at the lower end of the IoT telecom services market by enabling cost-effective connectivity for billions of utility meters, environmental sensors, asset trackers, and agricultural monitoring devices that require infrequent, low-bandwidth communication with multi-year battery life requirements. The transition from physical SIM card management to eSIM and iSIM remote provisioning is reducing enterprise IoT deployment friction and enabling global device fleet management at scale – a capability driving significant managed connectivity service adoption across multinational industrial and logistics operators.

Enterprise investment in private 5G network deployments for factory automation, port logistics, and campus connectivity is generating a new high-value service category within the IoT telecom services market forecast period, as telecom operators provide network design, spectrum licensing support, and managed service delivery for mission-critical industrial IoT environments. This investment pattern is reinforced by hyperscale cloud providers forming strategic alliances with telecom operators to deliver integrated IoT connectivity and cloud processing services through unified commercial frameworks, further expanding the market growth analysis horizon through 2033.

Get a free sample report: https://datahorizzonresearch.com/request-sample-pdf/iot-telecom-services-market-49770

Why Choose Our IoT Telecom Services Market Research Report

Our IoT telecom services market research report is engineered for telecom strategy executives, enterprise connectivity procurement leaders, infrastructure investors, and technology platform developers who require analytically rigorous, commercially actionable market intelligence rather than generalized telecommunications trend analysis. Grounded in primary research, structured expert interviews with telecom operator IoT business unit leaders and enterprise connectivity architects, and proprietary bottom-up revenue modeling, this report delivers a verified, comprehensive view of current market dynamics and long-range growth trajectories across the IoT telecom services market.

The competitive landscape analysis profiles 30+ active telecom operators and IoT connectivity platform providers across network technology capability, geographic coverage footprint, enterprise service portfolio depth, eSIM and connectivity management platform sophistication, and strategic partnership ecosystem strength – giving investors and commercial teams the structured benchmarking framework needed to evaluate market positioning within the IoT telecom services market. Segmentation is built at the precise intersection of connectivity technology, service type, industry vertical, device category, and geography, enabling identification of the highest-margin, fastest-growing demand clusters within current market share distribution.

Scenario-based forecasting accounts for 5G spectrum auction timelines, private network regulatory framework evolution, enterprise IoT budget cycle variability, and hyperscaler partnership dynamics that introduce meaningful uncertainty into the IoT telecom services market forecast. For telecom operators evaluating IoT service portfolio expansion, investors assessing connectivity infrastructure asset valuations, and enterprises selecting global managed IoT connectivity partners, this report delivers the strategic intelligence depth needed to act with precision and conviction.

Top Reasons to Invest in the IoT Telecom Services Market Report

• Comprehensive revenue forecasting across 2025-2033 supports confident network capacity investment, service portfolio development, and enterprise connectivity contract structuring decisions within the IoT telecom services market

• Segment-level growth analysis by connectivity technology, service type, industry vertical, and region identifies the highest-return investment opportunities and capability expansion priorities across the IoT telecom services market forecast period

• 5G, eSIM, private network, and edge computing technology trend mapping ensures telecom operators and enterprise technology investors understand which infrastructure and platform innovations are generating the strongest adoption momentum across the IoT telecom services market competitive landscape

• Competitive benchmarking intelligence covering operator network capability, pricing architecture, enterprise service portfolio depth, and partnership ecosystem quality equips commercial and strategy teams to strengthen market positioning and win high-value enterprise IoT connectivity mandates

• Regulatory spectrum policy and data governance analysis prepares regulatory affairs and network planning teams for evolving IoT connectivity licensing frameworks, spectrum allocation decisions, and cross-border data transfer compliance requirements affecting the IoT telecom services market across major economies

• M&A, joint venture, and strategic partnership opportunity identification supports infrastructure investors and telecom conglomerates in locating high-value IoT connectivity platform acquisitions and network infrastructure consolidation plays within the growing IoT telecom services market

IoT Telecom Services Market Challenges, Risks, and Barriers

Despite its exceptional growth trajectory, the IoT telecom services market faces substantive structural and operational challenges that operators and enterprise buyers must navigate with deliberate strategic planning. Spectrum availability constraints and the high capital expenditure requirements of 5G network densification limit the pace of coverage expansion, particularly in rural and emerging market geographies where IoT connectivity demand is growing fastest. Revenue monetization complexity – converting large connected device volumes into profitable managed service relationships – remains a persistent challenge for operators accustomed to traditional subscription revenue models. IoT device cybersecurity vulnerabilities expose network infrastructure to distributed attack vectors that create both reputational and operational risk. Additionally, fragmented global IoT connectivity standards and regulatory roaming frameworks complicate multinational enterprise deployment programs, extending procurement timelines within the IoT telecom services market growth analysis landscape.

Top 10 Companies in the IoT Telecom Services Market

• Ericsson AB

• Nokia Corporation

• Huawei Technologies Co., Ltd.

• Verizon Communications Inc.

• AT&T Inc.

• Deutsche Telekom AG

• Vodafone Group PLC

• China Mobile Limited

• Telefónica S.A.

• Telit Communications PLC

Market Segmentation

By Connectivity Technology:

o Cellular Technology

o Low Power Wide Area Network (LPWAN)

o Narrowband IoT (NB-IoT)

o Radio Frequency-Based (RF-Based)

By Service Type:

o Business Consulting services

o Device and Application Management services

o Installation and Integration services

o IoT Billing and Subscription Management

o M2M Billing Management

By Network Management Solution:

o Network Performance Monitoring and Optimization

o Network Traffic Management

o Network Security Management

By Application:

o Smart Building and Home Automation

o Capillary Network Management

o Industrial Manufacturing and Automation

o Vehicle Telematics

o Transportation and Logistics Tracking

o Energy and Utilities

o Smart Healthcare

o Others

By Region:

o North America

o Europe

o Asia Pacific

o Latin America

o Middle East & Africa

Recent Developments in the IoT Telecom Services Market

• Product Launch: Ericsson launched an enhanced IoT accelerator connectivity management platform in early 2025, incorporating AI-driven network slice optimization, automated eSIM lifecycle management, and real-time device fleet analytics capabilities targeting multinational enterprise clients across the IoT telecom services market

• Strategic Partnership: Vodafone Group announced a strategic collaboration with a leading hyperscale cloud provider in Q1 2025, establishing an integrated IoT connectivity and edge computing service offering that combines carrier-grade global network coverage with cloud-native data processing for industrial IoT enterprise clients

• Investment Round: A specialist IoT connectivity platform provider focused on satellite-cellular hybrid networks secured USD 245 million in Series D funding in late 2024, earmarked for global coverage expansion and enterprise-grade connectivity management platform development within the IoT telecom services market

• Geographic Expansion: Deutsche Telekom significantly expanded its NB-IoT and private 5G network coverage across Eastern Europe in 2025, enabling enterprise IoT deployments in Poland, Czech Republic, and Hungary to access carrier-grade managed connectivity services within the IoT telecom services market

• M&A Activity: Telefónica completed the strategic acquisition of a specialized IoT connectivity management software platform in 2025, integrating its multi-operator eSIM orchestration capabilities directly into Telefónica’s enterprise IoT service portfolio across Latin America and Europe

• Technology Upgrade: Nokia deployed a next-generation network slicing management system across its 5G standalone network infrastructure in 2025, enabling dynamic quality-of-service provisioning for critical industrial IoT applications including factory automation and autonomous guided vehicle connectivity

IoT Telecom Services Market Regional Performance & Geographic Expansion

North America leads the IoT telecom services market, driven by advanced 5G standalone network deployment progress, the highest enterprise IoT investment levels globally, and strong demand from manufacturing, automotive, healthcare, and smart infrastructure sectors across the United States and Canada. Europe holds the second-largest regional market share, with Germany, the United Kingdom, Sweden, and The Netherlands driving demand through industrial IoT adoption, private 5G campus network deployments, and stringent EU IoT cybersecurity and data governance compliance requirements. Asia-Pacific is the fastest-growing region within the IoT telecom services market, fueled by massive 5G network infrastructure investment in China, South Korea, Japan, and India alongside government-driven smart city and manufacturing digitalization programs. Latin America is emerging through cellular IoT expansion in Brazil and Mexico. The Middle East & Africa region is developing rapidly through smart city programs and 5G infrastructure investment in UAE, Saudi Arabia, and South Africa.

How IoT Telecom Services Market Insights Drive ROI Growth

Telecom operators, enterprise connectivity buyers, infrastructure investors, and IoT platform vendors that leverage authoritative IoT telecom services market intelligence consistently translate data into superior network investment decisions, enterprise client acquisition strategies, and competitive service positioning outcomes. Verified market share analysis across connectivity technologies, industry verticals, and geographies reveals where operators are gaining enterprise mandate wins and where unmet connectivity demand remains underserved by current network infrastructure and service portfolio coverage – enabling operators to prioritize capital deployment toward the highest-return network expansion and service development opportunities.

Segment-level revenue forecasting from this IoT telecom services market report equips network planning and commercial leadership teams with the demand validation needed to size capacity investments accurately, structure competitive enterprise connectivity contracts, and evaluate geographic expansion timing against verified IoT deployment growth trajectories. For infrastructure investors and private equity firms assessing telecom asset valuations or IoT platform acquisition opportunities, the forecast leverage embedded within this growth analysis provides the quantitative foundation for building investment conviction within the IoT telecom services market. Competitive benchmarking intelligence accelerates partnership negotiation, vendor qualification, and go-to-market execution for all stakeholder categories across this rapidly expanding market competitive landscape.

Sustainability & Regulatory Outlook

The IoT telecom services market is being shaped by an accelerating convergence of sustainability imperatives and an increasingly complex global regulatory environment that is directly influencing network infrastructure investment decisions, spectrum policy frameworks, and IoT device security design standards across every major geography. On the sustainability front, the energy consumption of IoT telecom network infrastructure – encompassing base stations, core network equipment, data centers, and edge computing nodes – is attracting significant scrutiny from both corporate sustainability programs and national energy efficiency regulators. Telecom operators within the IoT telecom services market are responding through aggressive renewable energy procurement for network infrastructure power supply, deployment of energy-efficient radio access network equipment, AI-driven network load optimization that reduces idle power consumption, and transition to more energy-efficient IoT connectivity protocols including NB-IoT, which consumes a fraction of the power of legacy cellular IoT technologies.

The growing scale of electronic waste generated by IoT device deployments – including connected sensors, asset trackers, smart meters, and industrial IoT hardware – is entering the regulatory agenda across Europe, North America, and Asia-Pacific, with extended producer responsibility frameworks beginning to impose device recyclability and take-back obligations on manufacturers and network service providers within the IoT telecom services market competitive landscape.

On the regulatory front, IoT device cybersecurity is the most consequential compliance driver reshaping service design requirements across the IoT telecom services market. The EU Cyber Resilience Act mandates security-by-design requirements and ongoing vulnerability management obligations for connected devices and the network service platforms that support them, directly affecting telecom operators providing managed IoT connectivity services across European markets. In the United States, the FCC’s IoT cybersecurity labeling program and NIST IoT security guidelines are establishing baseline security standards that enterprise procurement teams are beginning to incorporate into connectivity vendor qualification criteria. Spectrum regulatory evolution – including the ongoing development of licensed and unlicensed spectrum frameworks for private 5G networks and LPWAN IoT deployments – is creating both opportunity and complexity for operators positioning within the IoT telecom services market forecast horizon. Organizations that embed cybersecurity compliance, sustainable network operations, and spectrum regulatory expertise into their service delivery architecture are positioned to command premium enterprise partnerships and sustained competitive advantage through 2033.

Key Questions Answered in the Report

1. What is the projected revenue forecast for the IoT telecom services market through 2033, and which connectivity technologies, service categories, and industry verticals are generating the strongest growth momentum across the forecast period?

2. Which region will dominate the IoT telecom services market during the forecast period, and what 5G deployment pace, enterprise digitalization investment, and spectrum regulatory dynamics are shaping regional performance differentiation?

3. What are the highest-margin segments within the IoT telecom services market by connectivity type, service model, end-user industry, and geographic market, and how are these evolving as private 5G, eSIM, and edge computing service adoption intensifies?

4. Who are the emerging challengers most likely to disrupt established telecom operators across the IoT telecom services market competitive landscape, and what network technology, platform innovation, or pricing strategies are powering their growth?

5. How are IoT cybersecurity regulations, spectrum policy evolution, data sovereignty mandates, and sustainable network operation requirements reshaping infrastructure investment priorities and service design standards across the IoT telecom services market forecast horizon?

6. What M&A activity patterns, hyperscaler partnership structures, and private network deployment strategies are generating the strongest market share gains and strategic value for participants across the IoT telecom services market?

Contact:

Ajay N

Ph: +1-970-633-3460

Latest Reports:

Contact Lens Solution Market: https://datahorizzonresearch.com/contact-lens-solution-market-39704

Player Tracking Market: https://datahorizzonresearch.com/player-tracking-market-40380

Bodyshop Management Software Market: https://datahorizzonresearch.com/bodyshop-management-software-market-41057

Library Management Systems Market: https://datahorizzonresearch.com/library-management-systems-market-41733

Company Name: DataHorizzon Research

Address: North Mason Street, Fort Collins,

Colorado, United States.

Mail: sales@datahorizzonresearch.com

DataHorizzon is a market research and advisory company that assists organizations across the globe in formulating growth strategies for changing business dynamics. Its offerings include consulting services across enterprises and business insights to make actionable decisions. DHR’s comprehensive research methodology for predicting long-term and sustainable trends in the market facilitates complex decisions for organizations.

This release was published on openPR.