Simulation Software Market

The simulation software market continues to serve as a strategic backbone for industries validating designs, predicting system behavior, and optimizing operations with minimal physical risk. As enterprises deepen their reliance on digital twins, AI-integrated modeling, and virtual prototyping, competition within the simulation ecosystem is intensifying. This article provides a strategic review of top companies, industry-wide SWOT dynamics, and emerging investment themes-without referencing market sizing, CAGR metrics, or forward-looking projections.

➤ Request Free Sample PDF Report @ https://www.researchnester.com/sample-request-1316

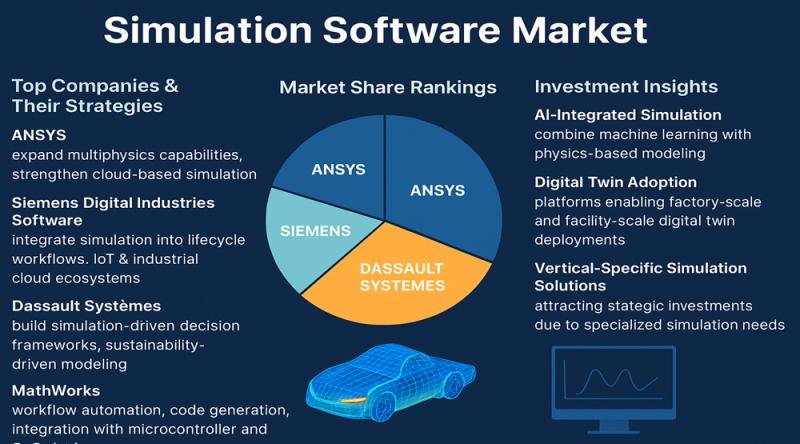

Top Companies & Their Strategies

1. ANSYS

ANSYS remains one of the most influential companies in the simulation software market, known for its physics-based simulation capabilities. Its strength lies in a broad portfolio spanning structural, thermal, fluid, and electromagnetics modeling. ANSYS’ strategy revolves around expanding multiphysics capabilities and strengthening cloud-based simulation through partnerships with hyperscalers. Its wide industry adoption-ranging from aerospace to consumer electronics-reinforces its global leadership.

2. Siemens Digital Industries Software

Siemens leverages its Xcelerator portfolio to integrate simulation into end-to-end product lifecycle workflows. The company’s strength is the deep integration of simulation with manufacturing execution systems and industrial automation. Siemens aggressively drives digital twin adoption, supported by its strong presence in Europe and Asia. Its strategy focuses on combining simulation with IoT and industrial cloud ecosystems.

3. Dassault Systèmes

Dassault Systèmes commands a strong position with its 3DEXPERIENCE platform, emphasizing collaborative simulation environments. Its CATIA and SIMULIA suites support complex engineering applications, especially in aerospace, automotive, and life sciences. The company’s strategic priority is building simulation-driven decision frameworks that integrate engineering, biology, and manufacturing. Dassault’s focus on sustainability-driven modeling also differentiates it in regulated industries.

4. MathWorks

MathWorks drives adoption in the simulation software market through its MATLAB and Simulink platforms. It excels in model-based design for control systems, autonomous systems, and embedded software. MathWorks continues to strengthen its position in academia and R&D labs, securing long-term user dependency. Its strategy emphasizes workflow automation, code generation, and integrations with microcontroller and SoC platforms.

➤ Get deeper insights into competitive positioning and strategic benchmarking: Download our sample Simulation Software Market report here → https://www.researchnester.com/sample-request-1316

5. Autodesk

Autodesk targets design-centric sectors with simulation tools embedded in AutoCAD and Fusion 360. Its competitive advantage lies in democratizing simulation capabilities for SMEs and design-focused professionals. Autodesk’s shift to cloud-native simulation and generative design supports faster iteration cycles. The company remains aggressive in enhancing usability, making simulation accessible to non-specialists.

6. Altair

Altair differentiates itself with strong capabilities in high-performance computing (HPC)-driven simulation and AI-enabled design optimization. Its HyperWorks platform is widely used in engineering-intensive industries. Altair’s strategy focuses on blending physics-based models with machine learning to accelerate product development cycles. Its global licensing flexibility and HPC strength attract cost-sensitive and compute-demanding users.

7. HEXAGON

HEXAGON leverages its manufacturing intelligence expertise to merge simulation with metrology, automation, and production validation. It is uniquely positioned in the simulation software market due to its digital manufacturing and smart-factory orientation. HEXAGON continues acquiring niche simulation players to enhance vertical-specific capabilities. Its focus is aligning virtual modeling with real-world measurement data to improve accuracy.

8. ESI Group

ESI Group is known for virtual prototyping expertise, especially in automotive and heavy engineering. Its products eliminate the need for costly physical testing through predictive simulation. The company strengthens competitiveness through specialization in crash, safety, acoustics, and weld modeling. ESI’s focus is on immersive simulation and real-time decision support environments.

➤ View our Simulation Software Market Report Overview here: https://www.researchnester.com/reports/simulation-software-market/1316

SWOT Analysis

Strengths

Leading companies in the simulation software market benefit from deep technical expertise and well-established product ecosystems. Their tools cover a wide range of engineering physics, enabling comprehensive modeling across industries. Most players also have strong global footprints, enhancing customer trust and ensuring diversified revenue streams. Partnerships with cloud providers, academia, and hardware vendors further reinforce industry dominance.

Weaknesses

Despite strong capabilities, many simulation solutions come with high licensing costs, restricting adoption among smaller firms. The steep learning curve of advanced simulation platforms also limits accessibility for non-engineering users. Integration challenges persist, particularly when combining legacy systems with modern simulation workflows. In addition, dependency on specialized talent hampers scalability for enterprise-wide deployment.

Opportunities

The rise of digital twins, AI-driven modeling, and cloud-native simulation creates substantial room for expansion. Emerging sectors-such as autonomous systems, renewable energy, and biotech-require sophisticated simulation environments. There is growing demand for real-time and edge-based simulation to support robotics, industrial automation, and smart-city applications. Increasing public and private investments in R&D further widen innovation pathways for software developers.

Threats

Competition is intensifying as new startups introduce low-cost or open-source alternatives targeting niche use cases. Rapid technological change could make certain legacy simulation methods obsolete. Cybersecurity risks associated with cloud-based simulation environments also present vulnerabilities. Furthermore, regulatory changes in sectors like aerospace or medical devices may increase compliance burdens for simulation vendors.

➤ Interested in a customized SWOT for your target competitor? Request your tailored assessment → https://www.researchnester.com/sample-request-1316

Investment Opportunities & Trends

Key Investment Themes

Investment momentum in the simulation software market is clustering around three major themes:

1. AI-Integrated Simulation: Investors are backing companies that combine machine learning with physics-based modeling to reduce computational load and accelerate validation cycles.

2. Digital Twin Adoption: Funding is flowing into platforms enabling factory-scale and facility-scale digital twin deployments, especially in manufacturing, energy, and infrastructure.

3. Vertical-Specific Simulation Solutions: Niche sectors such as autonomous mobility, semiconductor design, and biomedical engineering are attracting strategic investments due to specialized simulation needs.

Segments & Regions Attracting Capital

Sectors such as automotive, aerospace, electronics, and healthcare are seeing the strongest investment attention due to high engineering complexity. Regionally, North America and Europe continue to dominate in enterprise simulation adoption, while Asia-Pacific, driven by manufacturing growth and engineering R&D hubs, is emerging as a high-potential investment destination.

Notable Moves in the Last 12 Months

• Synopsys-Ansys Deal Completed: After regulatory clearance (e.g., from China), Synopsys completed the $35B acquisition of Ansys, forming a powerhouse across EDA and multiphysics simulation.

• Siemens-Altair Acquisition: Siemens’ takeover of Altair consolidates its simulation and analytics capabilities, reinforcing its industrial software strategy.

• Ansys Product Innovation: Ansys rolled out enhancements in Twin Builder, including TwinAI, which uses hybrid analytics and ROMs for smarter digital twin deployment.

• Altair HyperWorks Update: The latest HyperWorks 2025.1 release introduces better AI-driven optimization and faster physics simulations via reduced-order modeling.

• Autodesk CFD Advances: Autodesk added enhanced remote solving, browser-based simulation review, and one-click setup in its Simulation CFD suite to broaden access to simulation workflows.

➤ Request Free Sample PDF Report @ https://www.researchnester.com/sample-request-1316

Related News:

https://www.linkedin.com/pulse/how-extended-reality-changing-way-we-work-live-biohealth-trends-ipbgf/

https://www.linkedin.com/pulse/device-service-market-next-big-thing-tech-enterprises-llvzf/

Contact Data

AJ Daniel

Corporate Sales, USA

Research Nester

77 Water Street 8th Floor, New York, 10005

Email: info@researchnester.com

USA Phone: +1 646 586 9123

Europe Phone: +44 203 608 5919

About Research Nester

Research Nester is a one-stop service provider with a client base in more than 50 countries, leading in strategic market research and consulting with an unbiased and unparalleled approach towards helping global industrial players, conglomerates and executives for their future investment while avoiding forthcoming uncertainties. With an out-of-the-box mindset to produce statistical and analytical market research reports, we provide strategic consulting so that our clients can make wise business decisions with clarity while strategizing and planning for their forthcoming needs and succeed in achieving their future endeavors. We believe every business can expand to its new horizon, provided a right guidance at a right time is available through strategic minds.

This release was published on openPR.