Market Overview

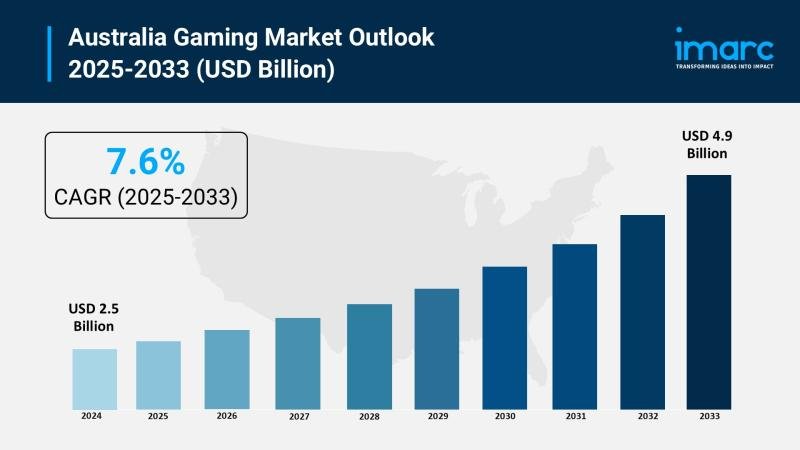

The Australia gaming market was valued at USD 2.5 Billion in 2024 and is expected to reach USD 4.9 Billion by 2033. The market growth is supported by factors such as the increasing adoption of mobile and console gaming, rising penetration of high-speed internet connectivity including 4G and 5G networks, and the growing availability of digital gaming platforms. Additionally, continuous innovation in gaming technologies, cloud gaming services, and immersive content is strengthening user engagement across diverse age groups. The forecast period spans 2025 to 2033, exhibiting a compound annual growth rate (CAGR) of 7.6%.

Grab a sample PDF of this report: https://www.imarcgroup.com/australia-gaming-market/requestsample

How AI is Reshaping the Future of Australia Gaming Market

• AI technologies enable adaptive gameplay by dynamically adjusting difficulty levels, environments, and game mechanics based on player behavior and skill levels, enhancing personalized gaming experiences.

• Advanced machine learning algorithms support procedural content generation, automated testing, and quality assurance, helping developers reduce development time and costs while improving creativity.

• AI-powered non-player characters (NPCs) exhibit more realistic and responsive behaviors, creating immersive and engaging in-game environments.

• AI-driven analytics tools assist developers in analyzing player data to optimize game design, monetization strategies, and content updates.

• Generative AI tools are increasingly used in game development workflows to create character designs, environments, narratives, and animations.

• Integration of AI with cloud gaming platforms improves performance optimization, latency management, and streaming quality, expanding access to high-end gaming across devices.

Market Growth Factors

The Australia gaming market is witnessing steady growth due to the rapid proliferation of smartphones, tablets, and gaming consoles, along with widespread availability of high-speed internet and expanding 4G and 5G networks across the country. Improved network infrastructure enables seamless online multiplayer gaming, cloud gaming, and real-time content streaming, enhancing overall user experience. Continuous advancements in hardware performance, graphics processing, and immersive technologies such as virtual reality (VR) and augmented reality (AR) are further contributing to higher engagement levels and longer playtime among gamers.

The rising popularity of gaming among younger demographics, including millennials and Generation Z, is another major growth driver. These consumer groups actively engage with mobile, console, and PC games across diverse genres, ranging from casual and social games to competitive multiplayer titles. The increasing influence of social media, live-streaming platforms, and online gaming communities is strengthening player interaction, encouraging content creation, and expanding audience reach, which supports sustained user growth across the market.

Commercialization and monetization opportunities are expanding rapidly in the Australia gaming market. Game developers and publishers are increasingly adopting flexible revenue models such as free-to-play with in-app purchases, subscriptions, downloadable content (DLC), and battle passes. In addition, the growth of esports tournaments, sponsorships, advertising partnerships, and collaborations between international publishers and local studios is generating new revenue streams and reinforcing gaming as a mainstream form of digital entertainment.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/australia-gaming-market

Market Segmentation

Device Type Insights:

• Mobile Gaming

• Console Gaming

• PC Gaming

Platform Insights:

• Online Gaming

• Offline Gaming

Revenue Model Insights:

• Free-to-Play Models

• Pay-to-Play Models

• In-App Purchases and Subscriptions

Age Group Insights:

• Below 18 Years

• 18-25 Years

• 26-35 Years

• 36-45 Years

• Above 45 Years

Regional Insights:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Key Players

• Tencent Games

• Activision Blizzard

• Electronic Arts (EA)

• Microsoft (Xbox)

• Sony Interactive Entertainment (PlayStation)

• Nintendo

• Local developers and studios

Recent Development & News

August 2025: The rollout of 5G infrastructure across major Australian cities expanded access to high-performance mobile and cloud gaming platforms, improving latency and enhancing online gaming experiences.

June 2025: Sony and Microsoft increased collaboration with Australian developers to introduce localized and exclusive gaming content, supporting regional developer ecosystems.

March 2025: Industry analysis indicated a rise in cloud gaming subscriptions and digital in-game purchases, reflecting changing consumer preferences toward flexible gaming models.

Note: Our reports database is continuously updated for the period 2025-2033 to reflect the latest market developments, emerging trends, demand dynamics, and growth insights. For access to the most current and comprehensive analysis, we invite you to request a sample report. One of our industry experts will connect with you shortly to discuss your specific requirements.

Speak to an analyst for a customized report sample PDF: https://www.imarcgroup.com/request?type=report&id=21962&flag=C

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers create a lasting impact. The company provides a comprehensive suite of market entry and expansion services, including market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.