The AI data centre market refers to a specialized segment of data centre infrastructure designed to support artificial intelligence (AI) workloads such as machine learning (ML), deep learning (DL), natural language processing (NLP) and real time analytics. These facilities are optimized with high performance computing hardware (like GPUs, TPUs and AI accelerators), advanced cooling systems, powerful networking, and software tools that can handle massive computational demands.

AI data centres are critical to the future of digital transformation. They serve as the backbone for cloud computing, big data analytics, generative AI, autonomous systems, and other technologies that require vast amounts of processing power and speed. Unlike traditional data centres, AI data centres are purpose built to process, analyze, and store extraordinary volumes of AI generated data efficiently and securely.

Download Free Sample@ https://www.cervicornconsulting.com/sample/2409

________________________________________

Market Size and Growth Outlook

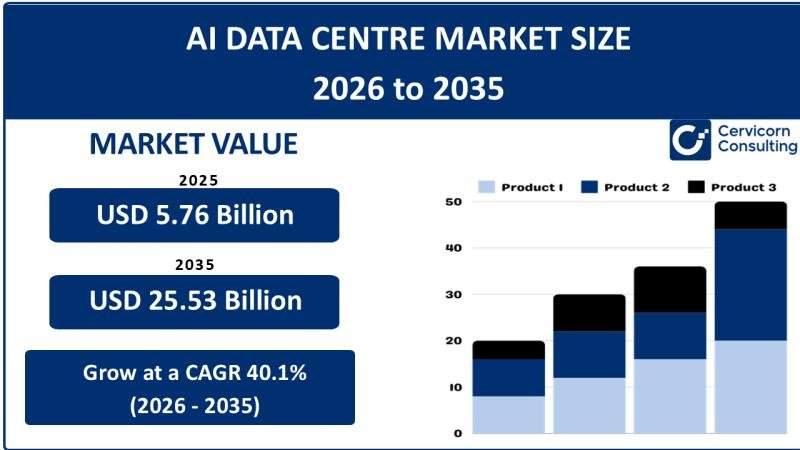

According to the Cervicorn Consulting report, the global AI data centre market was valued at USD 5.76 billion in 2025 and is expected to reach USD 25.53 billion by 2035, expanding at a CAGR of 40.1% from 2026 to 2035.

This explosive growth reflects the rapid adoption of AI technologies in healthcare, finance, e commerce, autonomous vehicles, telecommunications, and government services. Companies and cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and others are investing heavily in AI focused infrastructure to support next generation computing workloads.

________________________________________

Current Market Trends

1. Hyperscale Data Centre Expansion

Hyperscale data centres-large facilities designed to support massive volumes of data and processing power-dominate the AI data centre market. In 2025, they accounted for more than 52% of revenue share, indicating a strong shift towards centralized, highly efficient AI capable infrastructure.

2. AI Powered Operational Automation

AI is increasingly used to optimize data centre operations, including cooling control, load balancing, and energy management. These AI driven systems can analyze real time data, adjust cooling and power resources automatically, and significantly reduce operational costs and human intervention.

3. Edge AI Integration

As real time data processing becomes critical-especially for applications like autonomous vehicles and industrial automation-edge data centres are emerging. These smaller, localized facilities bring computing closer to the point of data creation, reducing latency and improving responsiveness.

4. AI Enhanced Security Solutions

With rising cyber threats, AI data centres are increasingly deploying AI based security systems that can detect anomalies and potential breaches in real time, offering a proactive defense strategy for mission critical data.

5. Renewable Energy Integration

Given the vast energy consumption of AI data centres, integrating renewable energy sources like solar and wind is becoming a priority. AI systems can forecast energy production and consumption patterns to balance workloads and reduce carbon footprints.

________________________________________

Market Drivers

1. Rapid Digital Transformation

As businesses transform digitally, there’s an increasing need for powerful computing infrastructure capable of supporting AI, analytics, automation, and real time decision making. This upgrade cycle fuels demand for advanced AI data centres.

2. Growth of Cloud and Hybrid Computing

The widespread adoption of cloud services and hybrid deployment models encourages organizations to use scalable AI data centre capabilities without heavy upfront investments.

3. AI and Machine Learning Adoption Across Industries

AI applications across sectors-such as predictive maintenance in manufacturing, fraud detection in finance, and personalized medicine in healthcare-drive substantial demand for robust data centre infrastructure.

4. Big Tech Investments in AI Infrastructure

Major technology companies are investing billions in AI data centres. For example, industry data show large scale global investments in AI and infrastructure build outs by tech giants, reflecting strong market confidence.

5. Edge Computing and Real Time Processing Needs

For performance sensitive use cases like autonomous driving and augmented reality, data needs to be processed closer to the source, driving the growth of edge AI data centre deployments.

________________________________________

Market Restraints

1. Data Privacy and Security Concerns

AI data centres handle massive amounts of sensitive data, making privacy and cybersecurity critical concerns. Regulatory compliance across different regions complicates infrastructure rollout and operation.

2. High Operational Costs

Building and maintaining AI ready infrastructure requires significant capital, including specialized hardware, cooling technology, and power systems. Smaller enterprises may find the high upfront cost prohibitive.

3. Complex Integration with Legacy Systems

Integrating new AI capabilities with existing legacy systems can be technically complex and expensive, often requiring significant reengineering of workflows.

4. Energy and Environmental Challenges

AI workloads are highly energy intensive. The increasing demand for energy raises concerns about sustainability and grid capacity, particularly for large AI data centres.

________________________________________

Market Opportunities

1. Emerging Market Investments

Emerging economies are prioritizing digital infrastructure development, resulting in increased investments in AI data centres. These regions offer significant long term growth potential for new entrants and existing vendors.

2. Innovations in Cooling and Power Technologies

New technologies-such as liquid cooling, immersion cooling, and AI driven power management-offer opportunities for more sustainable and cost efficient AI data centre operations.

3. AI Native Workload Support

As generative AI and other intensive workloads become mainstream, there’s growing demand for infrastructure optimized specifically for AI training, inference, and real time analytics.

4. Hybrid and Multi Cloud Deployments

Flexible deployment models that combine on premises, cloud based, and hybrid setups enable organizations to scale AI workloads efficiently and cost effectively.

Download Free Sample@ https://www.cervicornconsulting.com/sample/2409

________________________________________

Market Segmentation

By Component

• Hardware: Includes servers, GPUs, TPUs, accelerators, networking, and storage devices. Hardware accounted for around 59% of revenue share in 2025, as it forms the core of AI processing capability.

• Software: AI platforms, orchestration tools, AI workflows, and data management solutions used to manage AI workloads.

• Services: Consulting, integration, deployment, managed services, and support.

By Data Centre Type

• Hyperscale Data Centres: The dominant segment (~52% share), driven by cloud service providers and AI supercomputing needs.

• Colocation Data Centres: Serve multiple tenants with shared infrastructure and AI tooling.

• Enterprise Data Centres: Internal AI infrastructure within corporations.

• Edge Data Centres: Smaller facilities closer to end users for real time processing.

By Technology

• Machine Learning (ML): The leading technology segment, with ~36% share in 2025.

• Deep Learning (DL): Requires intensive compute support.

• Natural Language Processing (NLP) and Computer Vision: Growing areas as AI use cases expand.

By Deployment Model

• Cloud Based: The largest deployment mode (~53% in 2025).

• On Premises: Offers greater control but higher costs.

• Hybrid: Flexible combination of on premises and cloud.

By End User

Key end users include technology & cloud service providers, BFSI, healthcare & life sciences, telecom, automotive, retail & e commerce, government, and energy & utilities.

________________________________________

Regional Market Insights

North America

North America leads the global AI data centre market, holding approximately 39.4% of revenue share in 2025. This leadership is driven by extensive AI research, heavy investments by cloud providers, and strong technology infrastructure.

Europe

Europe accounted for about 21.5% of the market in 2025, with strong AI adoption, sustainability goals, and digital transformation initiatives in countries like Germany, the UK, and France.

Asia Pacific

Asia Pacific is one of the fastest growing regions, with investments in AI infrastructure rapidly increasing in China, Japan, South Korea, and India.

LAMEA (Latin America, Middle East & Africa)

The LAMEA region shows growing interest in AI data centre solutions as digital infrastructure investments rise, though growth is comparatively moderate.

Get the Full Report @ https://www.cervicornconsulting.com/ai-data-centre-market

________________________________________

Key Market Players

Leading companies driving the AI data centre market include:

• NVIDIA Corporation

• Intel Corporation

• IBM Corporation

• Google LLC

• Microsoft Corporation

• Amazon Web Services (AWS)

• Alibaba Cloud

• Baidu, Inc.

• Advanced Micro Devices (AMD)

• Hewlett Packard Enterprise (HPE)

• Cisco Systems, Inc.

• Dell Technologies

• Tencent Cloud

• Fujitsu Limited

These companies are investing in innovation, cooling solutions, AI accelerators, and power efficient systems to lead the market.

________________________________________

Future Market Growth Potential

The AI data centre market has vast future potential as AI workloads become more complex and widespread. The rise of generative AI, big data analytics, real time decision systems, and automation will fuel continuous growth. Investments in sustainable infrastructure and next generation cooling (such as liquid or immersion cooling) will further enhance operational efficiency.

Moreover, the continued development of edge AI, hybrid cloud strategies, and AI native platforms will expand opportunities for specialized data centre solutions.

________________________________________

Frequently Asked Questions (FAQ)

1. What is the AI data centre market size?

The global AI data centre market was valued at around USD 5.76 billion in 2025 and is expected to reach USD 25.53 billion by 2035 at a CAGR of ~40.1%.

2. What are AI data centres?

AI data centres are specialized facilities equipped with high performance computing hardware and software to support AI workloads such as ML, DL, and real time analytics.

3. What’s driving the market growth?

Key drivers include AI adoption across industries, cloud adoption, big tech investments, and digital transformation.

4. Which region dominates the AI data centre market?

North America leads in market share, driven by technological infrastructure and cloud investments.

5. What are the main challenges?

Data privacy, integration with legacy systems, and energy sustainability are core challenges.

6. Who are the major companies?

Top players include NVIDIA, Intel, IBM, Google, Microsoft, AWS, and others.

________________________________________

Conclusion

The AI data centre market is poised for extraordinary growth through 2035, fueled by rising adoption of AI technologies, hyperscale infrastructure build outs, and digital transformation across industries. With a projected CAGR of 40%, this market offers substantial opportunities for technology providers, infrastructure investors, and end users seeking high performance computing capabilities.

Emerging trends such as edge computing, AI driven operations, and renewable energy integration will shape more efficient and sustainable data centre ecosystems. As organizations increasingly rely on artificial intelligence for mission critical workloads, AI data centres will remain at the heart of tomorrow’s digital world.

Buy now at a 15% discount price: https://www.cervicornconsulting.com/buy-now/2409

Office No – 609, 6th Floor, 129/A Dattawadi, Sinhgad Road, Pune – 411030, India

Cervicorn Consulting is a global market research and consulting firm that provides syndicated research reports, industry insights, and customized consulting services across multiple sectors. The company focuses on delivering strategic market intelligence to help organizations make informed business decisions and identify emerging growth opportunities.

This release was published on openPR.