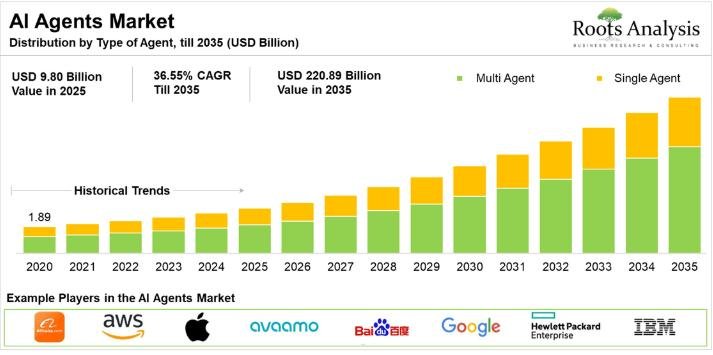

The global AI agents market, valued at USD 15 billion in 2026, will reach USD 221 billion by 2035, advancing at a CAGR of 34.64% over the forecast period, according to a new report by Roots Analysis. This 14-fold expansion reflects surging enterprise demand for automation, the rapid maturation of natural language processing technologies, and the accelerating push by organizations of all sizes to integrate autonomous software agents into core business workflows. For investors, technology vendors, and enterprise decision-makers, few markets in the current technology cycle offer this scale of growth with such broad cross-sector applicability.

To explore the complete findings, request a free sample of the report at https://www.rootsanalysis.com/ai-agents-market/request-sample

MARKET OVERVIEW

AI agents are autonomous or semi-autonomous software entities that use machine learning, natural language processing, and decision-making algorithms to execute tasks independently or in coordination with other systems. They are already deployed across customer service, healthcare, financial services, retail, and enterprise productivity, with adoption accelerating as foundation models become more capable and infrastructure costs fall.

The business case is straightforward: companies using AI agents report measurable reductions in operational cost, faster response cycles in customer-facing functions, and the ability to redirect human capital toward higher-order work. According to a Deloitte insight cited in the Roots Analysis report, by 2027 approximately 50% of companies using generative AI are expected to run agentic AI pilots or proofs of concept, up from 25% in 2025, a near-doubling in enterprise experimentation within two years.

Strategic alliances are already reshaping the supply side of this market. In October 2025, Oracle launched an AI Agent Marketplace inside its Fusion Cloud Applications, allowing partner-built agents to be delivered directly into enterprise workflows while supporting multiple leading foundation models. That same month, Hitachi advanced its partnership with Google Cloud to deploy field-specific agents for frontline workers, combining Hitachi’s domain expertise with Google Cloud’s generative AI infrastructure. In May 2025, Amazon Web Services partnered with Kore.ai to integrate its advanced AI agent platform into AWS services, enabling scalable and secure agent deployment for diverse business applications.

KEY GROWTH DRIVERS

Advances in Natural Language Processing NLP improvements are fundamentally expanding what AI agents can do. As models become better at understanding context, managing ambiguity, and generating fluent responses, agents are moving from narrow scripted functions toward genuinely adaptive interactions. This shift is directly expanding addressable use cases in customer service, healthcare triage, and enterprise knowledge management.

Enterprise Demand for Automation and Operational Efficiency Businesses are investing in AI agents to automate repetitive processes, reduce headcount in high-volume functions, and compress decision cycles. In BFSI, the pressure to automate fraud detection, risk assessment, and customer onboarding is particularly acute. The BFSI segment holds approximately 25% of the total market share in 2026, reflecting how deeply agentic automation has already penetrated financial services.

Hyper-Personalization at Scale Consumer-facing companies are using AI agents to deliver individualized experiences across chat, email, voice, and social media simultaneously. This capability, which would be cost-prohibitive with human agents alone, is a direct commercial driver of platform adoption, especially in retail and e-commerce where personalization directly correlates with conversion and retention.

Growth of Vertical AI Agents and Custom Deployments While ready-to-deploy horizontal agents dominate the market today (holding more than 85% share in 2026), build-your-own vertical agents are growing faster. Enterprises are finding that purpose-built agents, tailored to specific workflows and integrated with proprietary data systems, deliver substantially higher ROI than generic platforms. This trend is creating sustained demand for agent development infrastructure.

Multimodal Capabilities Expanding Agent Applications The move from text-only to multimodal AI agents, those capable of processing images, audio, documents, and structured data together, is opening new deployment categories in diagnostics, quality control, and real-time field operations. Healthcare, in particular, is benefiting from agents that can analyze patient data across formats to support clinical decision-making.

MARKET SEGMENTATION

The AI agents market breaks down across six primary dimensions: type of agent, technology, product type, agent role, end-use industry, and enterprise size. By agent type, single agents currently hold approximately 60% of the 2026 market, reflecting the relatively straightforward deployment of task-specific agents in enterprise settings. Multi-agent systems, which coordinate multiple specialized agents for complex problem-solving, are growing at the higher CAGR, driven by their superior performance in dynamic, multi-step workflows.

By technology, machine learning commands the largest share at roughly 40% in 2026, while natural language processing is the fastest-growing sub-segment given its centrality to conversational and generative AI applications. By agent role, research and summarization holds the highest share at approximately 25%, followed by productivity and personal assistants at 22%. Code generation is the fastest-growing role segment, fueled by the explosion in developer productivity tools and enterprise software development. In end-use industry, BFSI leads with about 25% share, but healthcare is growing at the highest CAGR, supported by digital health investment and government-backed AI adoption policies.

To request quote of this report, please visit:

https://www.rootsanalysis.com/ai-agents-market/request-quote

REGIONAL INSIGHTS

North America holds approximately 40% of the global AI agents market in 2026, a position the region is forecast to maintain through 2035, with roughly 75% of leading AI agent developers based in the region. The United States benefits from deep venture capital pools, the largest concentration of large language model developers globally, and an enterprise technology adoption culture that accelerates commercial deployment. Regulatory clarity, though still evolving, is further ahead in the United States than in most other markets, reducing compliance uncertainty for enterprise buyers.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 38.0% through 2035. The growth reflects massive government investment in AI research and development infrastructure across China, India, South Korea, and Japan, combined with rapid expansion of AI-native network infrastructure. The region’s large base of mid-sized manufacturers and consumer-facing enterprises provides a broad addressable market for both vertical and horizontal AI agent deployments.

COMPETITIVE LANDSCAPE

The AI agents market currently includes both global technology incumbents and a growing tier of specialized challengers. Key players identified in the Roots Analysis report include Alibaba, Amazon Web Services, Apple, Avaamo, Baidu, Google, Hewlett Packard Enterprise, IBM, Meta, Microsoft, NVIDIA, Oracle, Salesforce, SAP, and SoundHound, among others.

Close to 75% of leading developers offer agents with a primary role in customer service, reflecting where enterprise willingness to pay is currently highest. The competitive battleground is shifting toward model differentiation, agent orchestration capability, and the depth of pre-built integrations with enterprise software stacks. Smaller, specialized players such as Kasisto and Pandorabots are carving out positions in vertical niches, proving that incumbents do not yet own the market in sectors where domain specificity matters most. The surge in patent activity, with nearly 2,485 patents filed or granted in recent years, signals that IP accumulation is becoming a key strategic lever as the market matures.

Browse Full Report Description + Research Methodology + Table of Content + Infographics here:

https://www.rootsanalysis.com/ai-agents-market

Contact Details for Roots Analysis

Chief Executive: Gaurav Chaudhary

Email: Gaurav.chaudhary@rootsanalysis.com

Website: https://www.rootsanalysis.com/

About Roots Analysis

Roots Analysis is a global leader in the market research. Having worked with over 750 clients worldwide, including Fortune 500 companies, start-ups, academia, venture capitalists and strategic investors for more than a decade, we offer a highly analytical / data-driven perspective to a network of over 450,000 senior industry stakeholders looking for credible market insights. All reports provided by us are structured in a way that enables the reader to develop a thorough perspective on the given subject. Apart from writing reports on identified areas, we provide bespoke research / consulting services dedicated to serve our clients in the best possible way.

This release was published on openPR.