AI Accelerator Chip Market

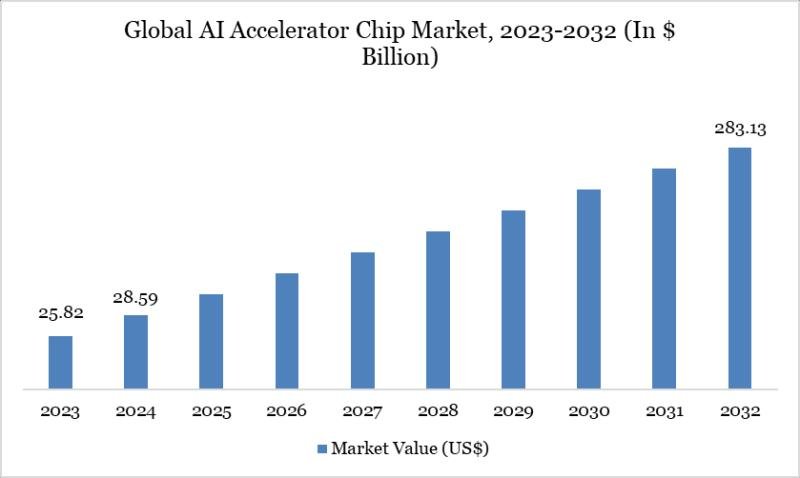

As per DataM intelligence research report “Global AI Accelerator Chip Market reached US$ 28.59 billion in 2024 and is expected to reach US$ 283.13 billion by 2032, growing with a CAGR of 33.19% during the forecast period 2025-2032.”

The market is growing rapidly with rising demand for high-performance computing and AI workloads. AI accelerator chips enhance processing speed and efficiency for machine learning tasks. Increasing adoption of AI across industries drives growth.

Download your exclusive sample report today: (corporate email gets priority access):

https://www.datamintelligence.com/download-sample/ai-accelerator-chip-market?prasad

Technological Advancements

✅ Feb 2026 – Next-Gen AI Chips Deliver Higher Processing Efficiency

Companies like NVIDIA and AMD are launching advanced AI accelerator chips with improved parallel processing and energy efficiency. These chips support large-scale AI model training and inference workloads. This enhances performance in data centers and edge computing applications.

✅ Jan 2026 – Custom AI Silicon for Cloud and Edge

Firms such as Google and Amazon Web Services are developing custom AI chips like TPUs and Inferentia. These solutions optimize AI workloads for cloud and edge environments. This reduces latency and operational costs.

✅ Oct 2025 – Integration of Advanced Packaging Technologies

Organizations including Intel and TSMC are adopting chiplet architectures and 3D packaging. These technologies improve performance density and scalability of AI accelerators. This supports next-generation computing requirements.

Product Launches & Innovations

✅ Feb 2026 – Launch of High-Performance Data Center AI Chips

Companies like NVIDIA introduced new GPUs optimized for generative AI and deep learning. These chips deliver higher throughput and memory bandwidth. This accelerates AI adoption across industries.

✅ Dec 2025 – Edge AI Accelerators for IoT Applications

Firms such as Qualcomm launched low-power AI chips for edge devices. These enable real-time AI processing in smartphones, automotive, and IoT systems. This expands AI capabilities beyond centralized infrastructure.

✅ Sep 2025 – AI Chips for Autonomous Systems

Companies including Tesla and Mobileye developed AI accelerators for autonomous driving. These chips process massive sensor data with high reliability. This supports safer and smarter mobility solutions.

Mergers & Acquisitions

✅ Jan 2026 – Strategic AI Chip Partnerships

Companies like Microsoft partnered with semiconductor firms to co-develop AI hardware. These collaborations aim to strengthen AI infrastructure capabilities. This enhances competitiveness in the AI ecosystem.

✅ Nov 2025 – Acquisition of AI Chip Startups

Major players such as Apple acquired AI semiconductor startups. These acquisitions boost in-house chip design capabilities. This supports innovation in consumer and enterprise devices.

✅ Oct 2025 – Collaborations for Advanced Semiconductor Manufacturing

Companies like Samsung Electronics and ASML are collaborating on advanced lithography solutions. These partnerships improve chip fabrication processes. This enables production of smaller and more powerful AI accelerators.

Ai accelerator chip Market: Competitive Intelligence

NVIDIA Corporation, Google Inc., Advanced Micro Devices Inc., Intel Corporation, Amazon Web Services Inc., Huawei Technologies Co. Ltd., Cerebras Systems Inc., Graphcore Limited, Qualcomm Incorporated, and SambaNova Systems Inc.

NVIDIA Corporation, Google Inc., Advanced Micro Devices Inc., Intel Corporation, Amazon Web Services Inc., Huawei Technologies Co. Ltd., Cerebras Systems Inc., Graphcore Limited, Qualcomm Incorporated, and SambaNova Systems Inc. are collectively driving the evolution of the AI Accelerator Chip Market by delivering high-performance processing solutions that optimize artificial intelligence workloads across cloud, edge, and enterprise applications. These companies develop specialized chips, including GPUs, TPUs, NPUs, and custom accelerators, designed to handle large-scale machine learning, deep learning, and inferencing tasks with improved speed, efficiency, and scalability. Through continuous innovation, expanded manufacturing capabilities, and strategic collaborations, they strengthen the adoption of AI-driven solutions and advance the growth of the AI Accelerator Chip Market globally.

Individually and collectively, these organizations’ strengths create competitive differentiation and momentum within the AI Accelerator Chip Market by combining technological leadership, architecture innovation, and ecosystem integration. NVIDIA Corporation and AMD lead in high-performance GPU solutions optimized for AI training and inferencing, while Intel Corporation and Qualcomm Incorporated provide versatile CPUs and AI accelerators for edge computing and hybrid architectures. Google Inc. and Amazon Web Services Inc. focus on cloud-based AI accelerators, including TPUs and managed services, to support large-scale AI deployments. Huawei Technologies Co. Ltd., Cerebras Systems Inc., Graphcore Limited, and SambaNova Systems Inc. advance novel architectures, high-throughput processing, and AI-specific hardware for specialized applications. Together, these companies combine performance, scalability, and system-level innovation to drive adoption and strengthen the AI Accelerator Chip Market.

Get Customization in the report as per your requirements: https://www.datamintelligence.com/customize/ai-accelerator-chip-market?prasad

Segment Covered in the Ai accelerator chip Market:

By Processing Type

The market is segmented into GPU-based 40%, CPU-based 25%, FPGA-based 20%, and ASIC-based 15%, with GPU-based chips dominating due to high parallel processing capabilities and strong adoption in AI training and inference tasks. FPGA and ASIC chips are growing rapidly for specialized, low-latency applications in data centers and edge devices. Increasing AI workloads across industries drive market growth.

By Chip Type

Chip types include discrete AI chips 55% and integrated AI chips 45%, with discrete chips dominating due to flexibility, high performance, and scalability for large-scale AI applications. Integrated chips are growing with adoption in consumer electronics, mobile devices, and embedded AI systems. Hardware optimization for AI workloads enhances adoption.

By Technology

Technologies include deep learning accelerators 50%, neural processing units (NPUs) 30%, vision processing units (VPUs) 10%, and others 10%, with deep learning accelerators dominating due to widespread AI adoption in computer vision, NLP, and autonomous systems. NPUs are gaining traction in mobile devices and edge AI applications. Continued AI innovation drives technology diversification.

By End-User

End-users include data centers 40%, automotive 25%, consumer electronics 15%, healthcare & life sciences 10%, and others 10%, with data centers dominating due to cloud AI, large-scale machine learning, and AI-as-a-Service adoption. Automotive and consumer electronics are growing with autonomous vehicles, smart devices, and robotics applications. Healthcare AI adoption is increasing for diagnostics and predictive analytics.

Buy Now & Unlock 360° Market Intelligence:

https://www.datamintelligence.com/buy-now-page?report=ai-accelerator-chip-market

Regional Analysis

North America – 35% Share

North America leads with 35% share driven by strong AI hardware development in United States and Canada. GPU-based and deep learning accelerators dominate. Data centers and automotive applications drive demand. Presence of major players such as NVIDIA, Intel, and AMD supports growth.

Europe – 25% Share

Europe holds 25% share with adoption in Germany, France, and United Kingdom. Discrete AI chips and deep learning accelerators dominate. Automotive and industrial AI applications drive demand. Government initiatives and AI R&D investments support growth.

Asia Pacific – 25% Share

Asia Pacific accounts for 25% share driven by adoption in China, Japan, and South Korea. GPU-based and NPU technologies dominate. Data centers, consumer electronics, and automotive sectors are key end-users. Increasing AI innovation, semiconductor manufacturing, and smart device adoption support growth.

Request for 2 Days FREE Trial Access:

https://www.datamintelligence.com/reports-subscription?prasad

✅ Competitive Landscape

✅ Technology Roadmap Analysis

✅ Sustainability Impact Analysis

✅ KOL / Stakeholder Insights

✅ Consumer Behavior & Demand Analysis

✅ Import-Export Data Monitoring

✅ Live Market & Pricing Trends

Contact Us –

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: Sai.k@datamintelligence.com

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

About Us –

DataM Intelligence is a Market Research and Consulting firm that provides end-to-end business solutions to organizations from Research to Consulting. We, at DataM Intelligence, leverage our top trademark trends, insights and developments to emancipate swift and astute solutions to clients like you. We encompass a multitude of syndicate reports and customized reports with a robust methodology.

Our research database features countless statistics and in-depth analyses across a wide range of 6300+ reports in 40+ domains creating business solutions for more than 200+ companies across 50+ countries; catering to the key business research needs that influence the growth trajectory of our vast clientele.

This release was published on openPR.