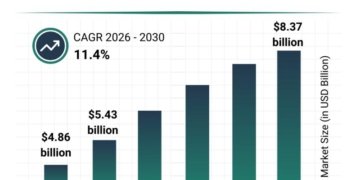

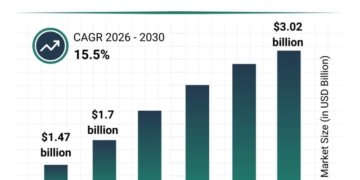

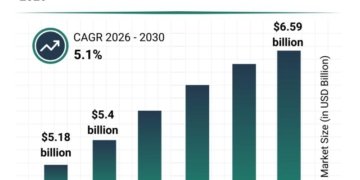

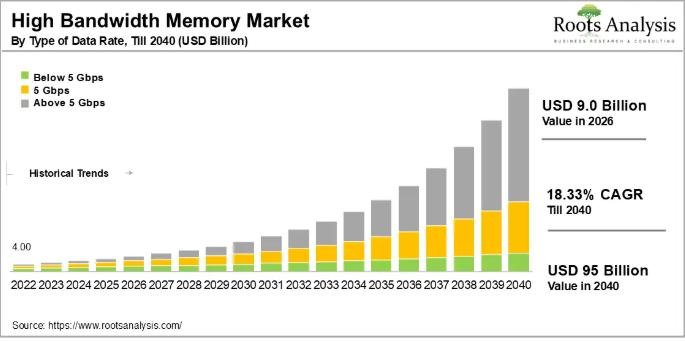

The global high bandwidth memory market, valued at USD 9.0 billion in 2026, will climb to USD 95 billion by 2040, advancing at a compound annual growth rate of 18.33% over the forecast period. That trajectory reflects surging demand from AI infrastructure, data center hyperscalers, and next-generation GPU platforms, making high bandwidth memory one of the fastest-scaling segments in the entire semiconductor industry.

To explore the complete findings, request a free sample of the report at https://www.rootsanalysis.com/high-bandwidth-memory-market/request-sample

Market Overview

High bandwidth memory is a 3D-stacked DRAM architecture that connects memory dies using through-silicon vias, positioning stacks directly beside processors such as GPUs, AI accelerators, and high-performance CPUs on a shared silicon interposer. This physical proximity eliminates the data movement bottlenecks that constrain conventional DDR memory, delivering bandwidth measured in terabytes per second while consuming substantially less power per transferred bit.

The timing of this technology’s ascent is not incidental. Foundation model training and inference at hyperscale require per-GPU memory bandwidth exceeding 3 TB/s, a threshold only HBM can reliably meet. SK Hynix projected in August 2025 that HBM would grow 30% annually through 2030, citing firm and strong end-user demand for AI memory. That forecast aligns with a string of notable corporate actions: in February 2026, Samsung began commercial shipments of sixth-generation HBM4, the first manufacturer to do so, while in March 2026 Samsung and AMD signed a memorandum of understanding covering HBM4 supply for AMD’s Instinct MI455X GPUs.

Government policy is also accelerating investment. Micron secured USD 6.1 billion in U.S. CHIPS Act funding to construct advanced DRAM fabrication facilities in New York and Idaho, adding domestic capacity specifically targeted at high-bandwidth products. Applied Materials and SK Hynix announced a long-term collaboration in March 2026 to advance next-generation DRAM and HBM at SK Hynix’s EPIC Center, further cementing the supply chain for future generations.

Key Growth Drivers

AI and Machine Learning Workload Expansion. Large language models and generative AI systems are now the primary demand engine for HBM. Training runs for frontier models consume massive memory bandwidth continuously, and cloud providers deploying these workloads at scale are designing server architectures around HBM availability rather than treating it as an optional upgrade.

3D and 2.5D Packaging Advances. Innovations in heterogeneous integration allow memory stacks to be placed in close proximity to logic dies on a silicon interposer, shrinking data travel distances while increasing effective bandwidth per watt. Mass production of HBM3, HBM3E, and HBM4 by SK Hynix, Samsung, and Micron now brings these architectures within reach for a wider range of system designs.

Data Center and Hyperscale Infrastructure Build-Out. Global cloud and colocation data center expansion drives sustained procurement of HBM-equipped accelerators. Data centers benefit from HBM’s ability to lower latency and reduce power consumption simultaneously, which directly cuts operating costs at scale. The servers application segment currently holds 32.76% of the HBM market, the largest of any application category.

Automotive and ADAS Adoption. Advanced driver-assistance systems require real-time sensor fusion across camera, LiDAR, and radar feeds. HBM’s compact 3D stacking supplies the throughput and low latency needed for in-vehicle AI inference without exceeding tight thermal and space budgets. The automotive and transportation end-user segment carries the fastest projected CAGR among all end-user categories at 23.12%.

Energy Efficiency at Data Center Scale. HBM delivers approximately 180 GB/s per watt and enables up to 30% power savings in data center memory subsystems compared with conventional DDR alternatives. As power and cooling costs become primary constraints in hyperscale facility design, this efficiency advantage is becoming a procurement criterion rather than a secondary consideration.

Market Segmentation

The high bandwidth memory market organizes across technology generation, memory capacity per stack, data rate, processor interface, architecture, application, and end-user industry. HBM3 currently holds the largest technology share at 34.67%, reflecting its widespread adoption in AI training accelerators and data center servers. HBM3E and the emerging HBM4 generation are growing fastest, projected at a CAGR of 23.34%, as manufacturers push stacking density and bandwidth ceilings through advanced TSV and 5D architecture designs.

Within processor interfaces, GPUs command 45.76% of current market share, sustained by their central role in both gaming and HPC workloads. The AI accelerator and ASIC segment is growing fastest at 23.12% CAGR, tracking the shift toward purpose-built inference chips from hyperscalers and chip startups. Memory capacity of 32 GB per stack and above represents the fastest-growing capacity tier at 22.89% CAGR, while data rates above 5 Gbps are both the dominant tier today and the fastest growing at 23.67% CAGR, driven by HBM3 and HBM3E adoption. On the application side, the graphics sub-segment is expanding fastest at a 23.22% CAGR, tied to demand for ultra-high-definition rendering and immersive extended-reality platforms.

To request quote of this report, please visit:

https://www.rootsanalysis.com/high-bandwidth-memory-market/request-quote

Regional Insights

Asia-Pacific holds the largest regional share of the high bandwidth memory market, accounting for over 32% of global revenues. South Korea anchors this position: SK Hynix and Samsung together control more than 80% of global HBM production capacity, and the Korean government has announced incentive programs supporting an expanded semiconductor fabrication cluster scheduled to open in 2027. Taiwan and China contribute additional manufacturing and packaging capacity within the region.

North America is the fastest-growing regional market, forecast at a CAGR of 22.85% through 2040. The combination of U.S. hyperscale cloud investment, AI model development concentrated among American technology companies, and Micron’s CHIPS Act-funded domestic fab expansion positions North America for significant share gains across the forecast window. Europe remains a secondary market but is actively building semiconductor policy frameworks aimed at reducing dependence on Asian supply chains over the longer term.

Competitive Landscape

The leading players in the high bandwidth memory market include SK Hynix, Samsung Electronics, Micron Technology, NVIDIA, Advanced Micro Devices, Intel, Broadcom, Fujitsu, Texas Instruments, Xilinx, and Open-Silicon.

SK Hynix currently leads with approximately 70% global HBM market share as of 2025, but that dominance is under active pressure. Samsung and Micron are both advancing next-generation HBM technologies and expanding production, with Samsung’s HBM4 commercial shipments in February 2026 representing the most direct competitive challenge to SK Hynix’s technology lead. The primary battleground is generational: whichever manufacturer achieves high-yield mass production of each successive HBM generation first secures preferential supply agreements with major GPU and accelerator designers. R&D intensity is high across all three companies, and partnerships with chip architects such as NVIDIA, AMD, and custom ASIC developers are becoming as strategically important as manufacturing scale.

Browse Full Report Description + Research Methodology + Table of Content + Infographics here:

https://www.rootsanalysis.com/high-bandwidth-memory-market

Contact Details for Roots Analysis

Chief Executive: Gaurav Chaudhary

Email: Gaurav.chaudhary@rootsanalysis.com

Website: https://www.rootsanalysis.com/

About Roots Analysis

Roots Analysis is a global leader in the market research. Having worked with over 750 clients worldwide, including Fortune 500 companies, start-ups, academia, venture capitalists and strategic investors for more than a decade, we offer a highly analytical / data-driven perspective to a network of over 450,000 senior industry stakeholders looking for credible market insights. All reports provided by us are structured in a way that enables the reader to develop a thorough perspective on the given subject. Apart from writing reports on identified areas, we provide bespoke research / consulting services dedicated to serve our clients in the best possible way.

This release was published on openPR.