Stratview Research

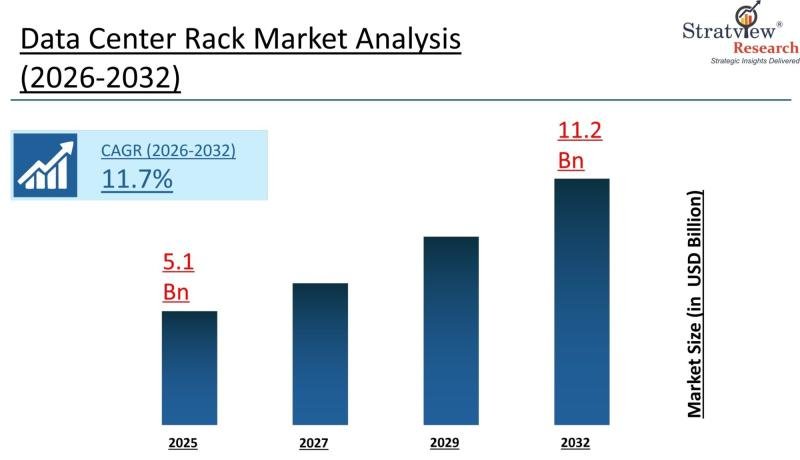

According to Stratview Research, the data center rack market projected to reach USD 5.8 billion in 2026 and is on a strong trajectory to reach USD 11.2 billion by 2032, growing at a CAGR of 11.7% during the forecast period of 2026-2032. The global data center rack market is experiencing a period of remarkable expansion, propelled by the accelerating adoption of cloud computing, artificial intelligence (AI), and edge computing. Data center racks – standardized metal cabinets designed to securely house and organize IT infrastructure such as servers and storage systems – have evolved significantly from traditional enclosures. New-generation racks now feature improved airflow management, liquid cooling readiness, and smart power distribution, enabling data center managers to handle the most demanding next-generation workloads.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4590/data-center-rack-market.html#form

Market Size & Forecast

The data center rack market recorded a market size of USD 4.5 billion in 2024. In 2025, the market experienced a year-over-year growth of 13%, reaching USD 5.1 billion. This upward trajectory is expected to continue, with the market projected to reach USD 5.8 billion in 2026 – an annual growth of 12.5% – before climbing to USD 11.2 billion in 2032. This represents a compound annual growth rate (CAGR) of 11.7% across the 2026-2032 forecast period. The cumulative sales opportunity during this period is estimated at USD 63.7 billion, which is nearly 1.94 times the annual demand in 2026, underscoring the significant long-term investment potential in this market.

Key Growth Drivers

Hyperscale and Cloud Expansion- The rapid growth of cloud computing services is among the most powerful drivers of the data center rack market. Hyperscale data centers demand standardized rack infrastructure capable of supporting the dense deployment of servers, storage systems, and networking equipment. Average rack power density has risen sharply – from 8-17 kW to over 30 kW – primarily due to the surge in AI and high-performance computing (HPC) workloads. Hyperscale facilities deploy thousands of racks to build the large compute clusters that underpin today’s digital services, creating sustained and growing demand for advanced rack solutions.

Edge Computing Infrastructure- The proliferation of low-latency IoT and 5G applications is driving the deployment of edge computing data centers, which in turn is creating strong demand for smaller, modular, and ruggedized rack systems. These racks are purpose-built for distributed, space-constrained environments. Typical edge deployments range from micro edge sites with 1-5 racks and total power up to 20 kW, to network edge hubs with 4-8 racks delivering 8-14 kW per rack, and larger edge data centers with 12-49+ racks operating at 12-14+ kW per rack. As edge infrastructure scales globally, the requirement for specialized rack solutions is accelerating alongside it.

Infrastructure And Density: Challenges and Opportunities:

High Initial Investment- One of the primary challenges constraining broader adoption of advanced data center racks is the high upfront capital cost. Specialized rack components integrated with advanced cooling and power solutions significantly increase infrastructure expenditure – particularly for small and medium-sized enterprises (SMEs) that lack the financial resources and scale of hyperscale operators. Hardware costs alone range from $1,000 to $5,000 per rack, excluding servers. When total deployment factors – including space, power, and cooling infrastructure – are considered, costs reach around $10-$12 million per megawatt (MW) for standard construction, while AI-optimized racks with high-density liquid cooling requirements can exceed $20 million per MW.

High-Density Power and Cooling Challenges- As AI and machine learning servers demand increasingly intense power loads, the resulting heat generation poses a fundamental design challenge. Traditional air cooling systems are no longer adequate for high-density environments, requiring racks to be purpose-built for liquid cooling compatibility. Integrating liquid cooling into existing data center architectures involves significant complexity, additional space requirements, and careful management of thermal limits – all of which must be balanced with the goal of maximizing computational density per rack.

Smart Rack Technology and Thermal Management Opportunities- The challenges of high-density computing are simultaneously creating compelling market opportunities. Smart rack technology – racks co-designed with advanced thermal, power, and liquid cooling solutions – allows data center managers to deliver significantly more computing workloads within the same physical footprint, at lower total cost of operation. Innovations include the delivery of high-density power solutions above 30 kW per rack, integration of advanced liquid thermal solutions, and the implementation of open rack standards that enable greater customization, security, and efficient deployment. These advancements make data center racks increasingly suitable for AI, cloud, and edge computing workloads, and are expected to serve as a key growth enabler throughout the forecast period.

Dominant Segments –

By Component Type – Cabinets & Enclosures Lead. The cabinets and enclosures segment is projected to dominate the data center rack market throughout the forecast period. These components provide essential structural support, protection, and efficient space management for IT equipment, making them foundational to modern data center infrastructure. As organizations continue expanding digital infrastructure and cloud capabilities, demand for advanced cabinets and enclosure systems will grow significantly, particularly across large-scale hyperscale and colocation data center deployments.

By Range Type – High-Density Racks (>30 kW) Drive the Future. The high-density racks segment (above 30 kW) is projected to be both the dominant and fastest-growing range type during the forecast period. This growth is directly driven by the rising adoption of AI and high-performance computing workloads, which demand racks engineered to support extreme power loads and advanced cooling requirements. The increasing deployment of AI servers and data-intensive applications across modern data centers is accelerating the transition from low- and medium-density racks to high-density solutions.

By Platform Type – Hyperscale Data Centers Outpace the Rest. The hyperscale data centers segment is anticipated to be the fastest-growing platform type during the forecast period. Major technology companies are investing heavily in hyperscale facilities to support expanding data storage demands, cloud computing workloads, and AI-driven applications. This large-scale expansion is significantly increasing the requirement for scalable, high-capacity rack infrastructure capable of supporting thousands of rack deployments per facility.

By Product Type – Server Racks Hold the Largest Share. Server racks are expected to hold the largest product-type market share throughout the forecast period. This dominance is driven by the increasing deployment of servers in cloud computing environments, enterprise IT infrastructure, and AI-powered applications. Server racks play a critical role in organizing and supporting server hardware while ensuring efficient airflow and thermal management – capabilities that become ever more essential as computational density rises.

Regional Leadership

Asia-Pacific is expected to be both the dominant and fastest-growing region in the data center rack market throughout the forecast period. The region’s strong position is primarily driven by rapid expansion of data center infrastructure, increasing cloud adoption, and substantial investments in digital transformation across key countries including China, India, Japan, and South Korea.

Asia-Pacific generated the highest demand with the largest market share in 2024, with China and India serving as the key engines of regional growth. The top 10 countries globally accounted for more than USD 4.10 billion – representing over 80% – of the global market value in 2025.

Top Players in the Data Center Rack Market

The data center rack market features a moderately consolidated competitive landscape, with the top 10 players collectively accounting for 50%-70% of global market share in 2025 (USD 2.5 billion to USD 3.5 billion). Most major players compete across key parameters including pricing, service offerings, product innovation, and regional presence. Leading manufacturers include:

• Schneider Electric

• Vertiv

• Legrand

• Rittal GmbH & Co.

• AMCO Enclosures

• HPC

• Dell Inc.

• Fujitsu

• nVent

• Eaton

• Cisco Systems

Conclusion: What Stratview Research Covers – and Why It’s Different

The data center rack market stands at a pivotal growth inflection, fueled by the convergence of AI, cloud computing, edge infrastructure, and escalating power density demands. From USD 5.1 billion in 2025 to a projected USD 11.2 billion by 2032, the market presents a cumulative opportunity of USD 63.7 billion that businesses cannot afford to navigate without precise, current intelligence.

This is exactly where Stratview Research delivers differentiated value. Unlike generic market research providers, Stratview Research’s Data Center Rack Market report covers five distinct market segments – component type, range type, platform type, product type, and region – with granular analysis across 15 countries and four major regions. The study period spans 2019-2032, providing both historical trend context and a rigorous forward-looking forecast. The report includes over 100 tables and figures, a competitive landscape analysis covering the strategic moves of all major players, Porter’s Five Forces analysis, SWOT assessment, and identification of the highest-growth market segments and associated investment opportunities.

400 Renaissance Center, Suite 2600,

Detroit, Michigan, MI 48243

United States of America

Website: http://www.stratviewresearch.com

Mail Us: sales@stratviewresearch.com

Press: media@stratviewresearch.com

Stratview Research is a global market research firm that highly specializes in aerospace & defense, chemicals, and a few other industries.

It launches a limited number of reports annually on the above-mentioned specializations. Thorough analysis and accurate forecasts in this report enable the readers to take convincing business decisions.

Stratview Research has been helping companies meet their global and regional growth objectives by offering customized research services. These include market assessment, due diligence, opportunity screening, voice of customer analysis, market entry strategies, and more.

This release was published on openPR.