Vendor Neutral Archive (VNA) and PACS Market

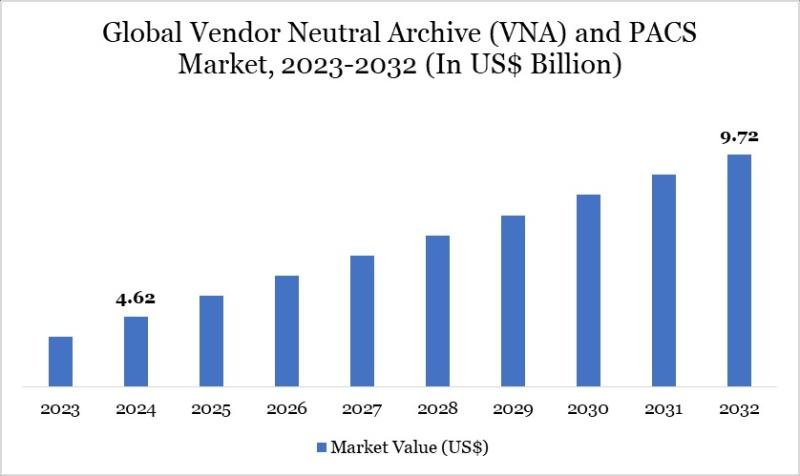

The global Vendor Neutral Archive (VNA) and PACS Market reached US$ 4.62 billion in 2024 and is expected to reach US$ 9.72 billion by 2032, growing at a CAGR of 9.75% during the forecast period 2025 to 2032. The market is expanding steadily due to the rising adoption of digital imaging technologies, increasing healthcare data volumes, and the need for efficient management and long term storage of medical images across healthcare systems.

The increasing requirement for universal medical image archiving, lower data storage costs, and seamless integration with electronic health record systems are major factors driving market growth. Vendor neutral archive solutions allow healthcare providers to store and access imaging data from multiple systems without vendor dependency, improving interoperability and clinical workflow efficiency. Growing digital transformation initiatives in healthcare, along with the rising demand for centralized imaging data management and advanced diagnostic capabilities, are further accelerating the adoption of VNA and PACS solutions globally.

Request Executive Sample report today: (corporate email gets priority access):https://www.datamintelligence.com/download-sample/vendor-neutral-archive-vna-and-pacs-market?sai-v

Vendor neutral archive and picture archiving and communication system solutions are becoming essential components of modern medical imaging infrastructure as healthcare providers transition toward fully digital and data integrated environments. These platforms enable the storage, management, and seamless sharing of large volumes of medical images across different imaging modalities and healthcare systems. By supporting interoperability and centralized image management, VNA and PACS solutions help hospitals and diagnostic centers improve clinical workflows, reduce data silos, and enhance collaboration among radiologists, physicians, and healthcare networks. The rapid growth of diagnostic imaging procedures, expansion of telemedicine services, and increasing adoption of cloud based healthcare IT platforms are accelerating market demand globally.

For healthcare executives, hospital administrators, and medical imaging technology providers, the vendor neutral archive and PACS ecosystem represents both a strategic IT investment and a critical step toward integrated patient care. Regulatory frameworks and data interoperability standards guided by organizations such as the Health Level Seven International and the Integrating the Healthcare Enterprise are shaping system architecture and data exchange protocols. Companies that prioritize scalable cloud storage, advanced analytics capabilities, and secure image sharing platforms are well positioned to improve diagnostic efficiency, strengthen clinical decision making, and build competitive advantage in the evolving digital healthcare landscape.

Key Developments

✅ February 2026: To improve interoperability and centralized medical imaging data management across healthcare networks, in North America and Europe, GE HealthCare expanded its enterprise imaging portfolio with enhanced Vendor Neutral Archive (VNA) capabilities and cloud enabled PACS integration to support multi hospital imaging workflows and long term data storage.

✅ January 2026: Driven by increasing demand for cloud based imaging platforms and remote diagnostics, in Asia Pacific, Fujifilm Holdings Corporation launched upgraded VNA and PACS solutions with AI assisted image management and improved interoperability for regional healthcare systems.

✅ December 2025: To streamline radiology workflows and improve diagnostic collaboration, in Europe, Philips Healthcare enhanced its enterprise imaging platform with scalable VNA architecture and integrated PACS analytics designed to support multi facility healthcare networks.

✅ November 2025: In response to rising demand for centralized medical image storage and cross platform access, in United States, Agfa HealthCare expanded its VNA and PACS offerings with advanced imaging data lifecycle management and improved cloud connectivity for hospitals and diagnostic centers.

✅ October 2025: To support healthcare digital transformation and enterprise wide imaging access, in Global Markets, Siemens Healthineers introduced advanced PACS solutions integrated with vendor neutral archiving systems and AI powered image analysis tools for improved clinical decision making.

✅ September 2025: Driven by increasing need for scalable imaging infrastructure and data interoperability, in Middle East and Asia, Canon Medical Systems strengthened its enterprise imaging solutions with upgraded VNA platforms and cloud ready PACS deployments for large healthcare institutions.

Competitive Landscape and Industry Partnerships

The global vendor neutral archive (VNA) and PACS market is characterized by the presence of healthcare technology providers, medical imaging companies, and enterprise IT solution providers focusing on interoperable imaging data management platforms. Leading participants include Agfa-Gevaert Group, Dell Technologies Inc., FUJIFILM Holdings Corporation, GE HealthCare, IBM Corporation, Koninklijke Philips N.V., Lexmark International Inc., McKesson Corporation, Novarad Corporation, and Siemens Healthineers AG. These companies compete through advanced medical imaging software, cloud based data archiving platforms, and interoperable healthcare IT systems.

Industry players are investing in cloud integrated VNA platforms, artificial intelligence driven image analytics, and secure data interoperability solutions to enhance clinical workflows and diagnostic efficiency. Strategic collaborations with hospitals, diagnostic imaging centers, and health information exchange networks are accelerating the adoption of enterprise imaging ecosystems. As healthcare providers increasingly prioritize centralized imaging storage, multi vendor interoperability, and data driven clinical decision making, VNA and PACS solution providers are expected to play a critical role in modernizing digital healthcare infrastructure worldwide.

Investment Outlook

The Vendor Neutral Archive (VNA) and Picture Archiving and Communication Systems (PACS) market is becoming increasingly competitive as healthcare IT vendors, imaging technology providers, and cloud infrastructure companies invest heavily in enterprise imaging platforms, interoperability standards, and AI-enabled diagnostic workflows. Major industry participants such as GE HealthCare, Siemens Healthineers, Koninklijke Philips N.V., FUJIFILM Holdings Corporation, and Agfa HealthCare are expanding enterprise imaging ecosystems that integrate radiology, cardiology, pathology, and other imaging departments into unified platforms. Vendors are focusing on cloud native architectures, AI powered image analytics, and advanced interoperability standards such as DICOM, HL7, and FHIR to enhance diagnostic efficiency and enable seamless data exchange across healthcare networks.

For C level executives and strategic investors, the VNA and PACS market represents a strong growth opportunity aligned with digital health transformation, increasing medical imaging volumes, and the global shift toward enterprise wide imaging systems. Healthcare providers are increasingly adopting cloud based VNA platforms to improve scalability, reduce infrastructure costs, and enable remote image access across multi site hospital networks. Organizations that invest early in scalable cloud infrastructure, cybersecurity compliance, AI driven imaging analytics, and integrated electronic health record connectivity are likely to capture substantial long term value as healthcare systems modernize imaging data management and diagnostic workflows.

Purchase Corporate License | Market Intelligence:https://www.datamintelligence.com/buy-now-page?report=vendor-neutral-archive-vna-and-pacs-market?sai-v

Market Drivers

– Increasing adoption of digital imaging technologies in healthcare facilities driving demand for efficient image storage and management solutions.

– Growing need for interoperability across healthcare systems encouraging adoption of vendor neutral archive platforms that enable seamless data sharing.

– Rising volume of diagnostic imaging procedures including CT, MRI, ultrasound, and X ray increasing the need for scalable image archiving systems.

– Expansion of telemedicine and remote diagnostics creating demand for centralized imaging access and cloud based PACS platforms.

– Advancements in healthcare IT infrastructure including cloud computing, artificial intelligence, and data analytics enhancing imaging workflow efficiency.

– Growing emphasis on reducing healthcare data silos and improving clinical collaboration across hospitals and diagnostic centers.

– Regulatory requirements and data management standards encouraging healthcare providers to adopt secure and compliant imaging storage systems.

Industry Developments

– Launch of advanced cloud based PACS and VNA platforms offering scalable storage, faster data retrieval, and improved interoperability.

– Strategic partnerships between healthcare IT providers, diagnostic imaging – vendors, and hospital networks to deliver integrated imaging management solutions.

– Development of AI enabled imaging analytics tools that assist radiologists in diagnosis, workflow optimization, and image interpretation.

– Expansion of enterprise imaging platforms that consolidate radiology, cardiology, pathology, and other imaging specialties into a unified system.

– Investments in cybersecurity and data protection technologies to ensure secure storage and transfer of sensitive medical images.

– Introduction of mobile and web based PACS viewers that enable clinicians to access imaging data remotely for faster clinical decision making.

Regional Insights

North America 40% share. “Driven by advanced healthcare IT infrastructure, widespread adoption of digital imaging systems, and strong demand for enterprise imaging platforms.”

Europe 27% share. “Supported by healthcare digitization initiatives, interoperability standards, and rising demand for centralized medical imaging archives.”

Asia Pacific 25% share. “Fueled by expanding healthcare infrastructure, increasing diagnostic imaging procedures, and growing investments in healthcare IT systems in China, India, Japan, and Southeast Asia.”

Latin America 5% share. “Boosted by improving healthcare digitization, expansion of diagnostic imaging services, and adoption of modern data management systems.”

Middle East & Africa 3% share. “Driven by healthcare infrastructure modernization, investments in hospital IT systems, and growing demand for digital medical imaging solutions.”

Request Custom Intelligence Report:https://www.datamintelligence.com/customize/vendor-neutral-archive-vna-and-pacs-market?sai-v

Key Segments

By Imaging Modality

Computed tomography imaging systems generate large volumes of diagnostic images and represent a major modality integrated with VNA and PACS platforms for efficient storage and retrieval. Magnetic resonance imaging systems are widely used for detailed soft tissue visualization, driving demand for advanced archiving and image management solutions. Ultrasound imaging is commonly used in obstetrics, cardiology, and abdominal diagnostics and requires reliable image storage and sharing capabilities. X ray imaging remains one of the most widely used diagnostic modalities, particularly in emergency and orthopedic settings. Mammography imaging systems generate specialized breast imaging data that require long term archiving and secure access. Nuclear imaging modalities such as PET and SPECT scans produce functional imaging data that benefit from integrated archiving platforms. Other modalities include fluoroscopy and digital pathology imaging systems.

By Type

Vendor Neutral Archive systems provide centralized storage and management of medical images from multiple imaging systems and vendors, enabling interoperability and long term data preservation. Picture Archiving and Communication Systems manage the acquisition, storage, retrieval, and sharing of medical images across healthcare facilities. Integrated VNA and PACS solutions are increasingly adopted to streamline imaging workflows, improve clinical collaboration, and reduce data silos across healthcare networks.

By Mode of Delivery

On premise deployment involves installing VNA and PACS infrastructure within healthcare facility data centers, providing direct control over data security and system management. Cloud based delivery models are gaining traction as they offer scalable storage, remote accessibility, and reduced infrastructure costs. Hybrid delivery models combine on premise and cloud capabilities, enabling healthcare providers to balance data control with flexible storage and disaster recovery options.

By Usage Model

Single site usage models are implemented within individual hospitals or diagnostic centers to manage imaging workflows locally. Multi site usage models are designed for healthcare networks and hospital groups, enabling centralized image management across multiple facilities. Enterprise wide usage models support large healthcare systems by integrating imaging data with electronic health records and other clinical information systems to enable comprehensive patient data management.

Unlock 360° Market Intelligence with DataM Subscription Services: https://www.datamintelligence.com/reports-subscription

Power your decisions with real-time competitor tracking, strategic forecasts, and global investment insights all in one place.

✅ Competitive Landscape

✅ Sustainability Impact Analysis

✅ KOL / Stakeholder Insights

✅ Unmet Needs & Positioning, Pricing & Market Access Snapshots

✅ Market Volatility & Emerging Risks Analysis

✅ Quarterly Industry Report Updated

✅ Live Market & Pricing Trends

✅ Import-Export Data Monitoring

Have a look at our Subscription Dashboard: https://www.youtube.com/watch?v=x5oEiqEqTWg

Contact Us –

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: Sai.k@datamintelligence.com

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

About Us –

DataM Intelligence is a Market Research and Consulting firm that provides end-to-end business solutions to organizations from Research to Consulting. We, at DataM Intelligence, leverage our top trademark trends, insights and developments to emancipate swift and astute solutions to clients like you. We encompass a multitude of syndicate reports and customized reports with a robust methodology.

Our research database features countless statistics and in-depth analyses across a wide range of 6300+ reports in 40+ domains creating business solutions for more than 200+ companies across 50+ countries; catering to the key business research needs that influence the growth trajectory of our vast clientele.

This release was published on openPR.