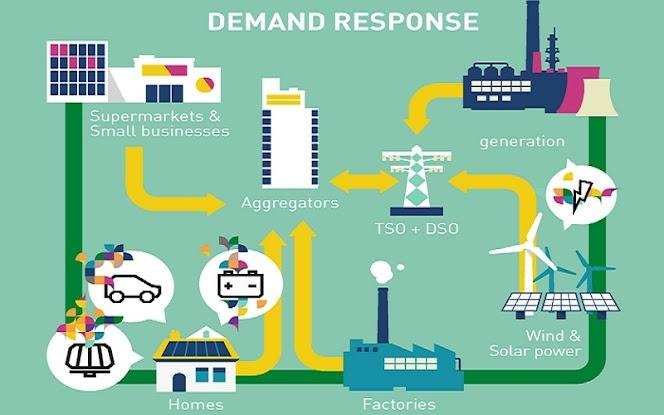

Demand Response Market

The global Demand Response (DR) Market is projected to expand from USD 35.2 billion in 2025 to USD 127.1 billion by 2035, registering a robust CAGR of 12.2% over the forecast period. The growth trajectory reflects accelerating investments in smart grid modernization, renewable energy integration, and digital energy management technologies that are transforming how electricity demand is monitored, managed, and optimized.

As electricity consumption patterns become increasingly dynamic-driven by rapid urbanization, industrial expansion, electrification, and distributed renewable generation-grid operators and utilities are prioritizing demand-side flexibility as a strategic necessity. Demand response programs enable residential, commercial, and industrial consumers to shift or reduce energy usage during peak demand periods in exchange for incentives, enhancing grid reliability while reducing operational and environmental costs.

Request For Sample Report | Customize Report | Purchase Full Report

https://www.futuremarketinsights.com/reports/sample/rep-gb-1287

Grid Resilience and Renewable Integration Driving Market Expansion

The integration of renewable energy sources such as solar and wind-characterized by intermittency and variability-has intensified the need for flexible load management systems. Demand response solutions allow utilities to balance supply and demand in real time, minimizing reliance on costly and carbon-intensive peaker plants.

Government-backed initiatives are reinforcing this shift. In 2024, the U.S. Department of Energy allocated USD 200 million to support grid modernization projects that combine renewable generation with demand response capabilities. Similar policy frameworks across Asia and Europe are accelerating adoption through incentives and compliance mandates.

The market’s expansion reflects a structural transition: grid stability is no longer dependent solely on generation capacity but increasingly on intelligent consumption management.

Services Segment Leads with Double-Digit Growth

Within the market structure, the Services (Solution) segment is forecast to grow at a CAGR of 14.3% from 2025 to 2035, outpacing overall market growth. Rising demand for real-time monitoring, automated load shifting, and predictive analytics is reshaping energy management strategies across utilities and enterprises.

AI-driven forecasting models, machine learning algorithms, and cloud-based automation platforms are enabling more accurate load balancing and demand prediction. Companies are deploying advanced analytics platforms that integrate smart meters, IoT sensors, and building management systems to automate consumption adjustments without disrupting operations.

In 2024, Schneider Electric introduced enhancements to its EcoStruxure platform, integrating demand response with real-time analytics to optimize energy performance in commercial facilities. These innovations demonstrate how software-centric solutions are becoming central to grid orchestration and operational efficiency.

As regulatory environments increasingly mandate participation in flexible load programs, service providers offering consulting, integration, monitoring, and automated demand response (ADR) capabilities are positioned for sustained growth.

Commercial Buildings Dominate End-User Adoption

Commercial buildings are expected to account for 27.8% of total market share in 2025, making them the leading end-user segment. Office complexes, retail centers, hotels, hospitals, data centers, and university campuses represent high-energy-density environments with substantial peak demand exposure.

By integrating smart meters, AI-powered building management systems, and automated HVAC optimization, commercial facilities can shift non-critical loads during peak pricing windows. Participation in demand response programs enables cost savings, improved sustainability metrics, and enhanced compliance with evolving climate-conscious regulations.

Regulatory frameworks are reinforcing this momentum. California energy regulators, for example, mandated automated demand response participation for commercial customers exceeding 500 kW in peak demand, resulting in a 30% increase in ADR engagement.

As cities adopt stricter decarbonization and efficiency mandates, commercial infrastructure will remain a cornerstone of demand-side energy optimization.

Country-Level Growth Highlights

Demand response adoption varies across regions, reflecting differences in policy support, infrastructure maturity, and digital readiness.

India (15.0% CAGR) leads growth, driven by large-scale smart meter deployment under the Revamped Distribution Sector Scheme (RDSS), which aims to replace 250 million conventional meters with smart meters by 2025.

China (14.2% CAGR) benefits from strong government investment in AI-driven smart grids, supported by over USD 10 billion allocated for digital grid infrastructure under the 14th Five-Year Plan.

United States (12.5% CAGR) advances through widespread ADR implementation and federal funding commitments, including USD 80 million allocated to demand-side programs in high-load states.

Japan (11.8% CAGR) and Germany (10.5% CAGR) are expanding through structured grid modernization programs and industrial energy optimization initiatives.

China currently accounts for approximately 42.8% of global market share, supported by rapid industrial growth and large-scale renewable integration.

Industrial and Commercial Energy Demand Intensifies Optimization Needs

Rising electricity consumption in manufacturing facilities, data centers, and logistics hubs is intensifying peak load pressures globally. Industrial facilities consuming more than 50 GWh annually in China are now required to participate in demand response programs under updated regulatory directives.

Advanced AI-enabled demand response platforms allow enterprises to automate energy adjustments based on real-time price signals, reducing operational costs while maintaining production continuity. As industrial electrification accelerates, demand-side optimization becomes integral to corporate energy strategies.

Exhaustive Market Report: A Complete Study

https://www.futuremarketinsights.com/reports/demand-response-market

Technology Innovation and Competitive Dynamics

The demand response market remains highly competitive, shaped by rapid advancements in automation, analytics, and distributed energy resource (DER) integration. Key industry participants include:

• Siemens AG

• Schneider Electric

• Honeywell International Inc.

• General Electric

• Eaton Corporation

• Itron Inc.

• Enel X

• AutoGrid Systems

• CPower Energy Management

• EnergyHub

Strategic partnerships and contract wins are reinforcing competitive positioning. In March 2024, Schneider Electric secured a USD 25 million, five-year contract with a regional utility to deploy advanced metering infrastructure and customer engagement platforms. Siemens AG followed with a USD 40 million, seven-year agreement in July 2024 to implement a comprehensive demand response management system integrating renewable energy sources and automated load balancing.

Additionally, in early 2025, Bandera Electric Cooperative partnered with Tesla to launch a virtual power plant program in Texas, illustrating the growing convergence of demand response and distributed energy storage systems.

Infrastructure Constraints and Digital Gaps

Despite strong growth, adoption challenges persist in developing regions where aging grid infrastructure, limited smart meter penetration, and insufficient IoT connectivity constrain real-time demand management. Grid digitization remains a prerequisite for large-scale deployment, requiring continued investment in communication networks, automation systems, and cloud-based analytics platforms.

However, as governments prioritize grid modernization to meet climate commitments and urban growth demands, infrastructure upgrades are expected to unlock additional market potential.

Long-Term Outlook

With global electricity systems undergoing structural transformation, demand response is emerging as a central pillar of grid modernization strategies. The projected rise to USD 127.1 billion by 2035 reflects not only regulatory momentum and renewable integration but also the evolution of intelligent, automated energy ecosystems.

As smart grids, AI-driven analytics, and distributed energy resources converge, demand response will play a defining role in ensuring grid reliability, operational efficiency, and environmental sustainability.

Comprehensive analysis of segment performance, regional policy impacts, technology benchmarking, and competitive positioning is detailed in the full market research report, offering strategic insights into one of the fastest-growing segments of the global energy management landscape.

Similar Industry Reports

Incident Response Market

https://www.futuremarketinsights.com/reports/incident-response-market

Biologic Response Modifiers Market

https://www.futuremarketinsights.com/reports/biologic-response-modifiers-market

Emergency Response and Rescue Vessels Market

https://www.futuremarketinsights.com/reports/emergency-response-and-rescue-vessels-market

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-845-579-5705

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

This release was published on openPR.